Fellow Investor,

Thanks to President Trump's America-First policies, a historic wave of investment is flooding back into the United States:

Apple committing a colossal $500 billion to build new U.S. factories.

Microsoft injecting $80 billion into domestic manufacturing.

Nvidia moving critical chip production back to America.

But here's the hidden opportunity:

There's now a groundbreaking way for you to start collecting monthly checks from these very same companies—checks that could reach as high as $5,917 each month.

Don't miss your chance to participate directly in America's industrial comeback.

Watch Now to Learn How to Get Your First Check in 30 Days

Tim Plaehn

Chief Income Strategist, Investors Alley

Copa Holdings May Be the Airline Stock Built to Break Out

Submitted by Thomas Hughes. Article Posted: 6/23/2026.

Key Points

- Copa Holdings has a lot going for it, making it a win for investors seeking growth and capital returns.

- A hub-and-spoke setup enables highly efficient airline operations.

- Analysts are forecasting this emerging market stock to reach new highs in 2026.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

Copa Holdings (NYSE: CPA) is an airline stock with structural advantages, a strong market position, and capital returns that make it a nearly perfect investment. Its positioning as a leading Latin American service provider offers emerging-market exposure in a critical infrastructure and services play. Its key structural advantage is a hub-and-spoke network centered on The Hub of the Americas. The Hub of the Americas is the company’s headquarters at Tocumen International Airport, a centralized location that enables ultra-efficient operations across the system.

This setup supports the region's leading service record and the No. 2 record globally, with an average on-time rate of about 90% and completion rates trending in the 99% range. In addition to the hub-and-spoke model, Tocumen's centralized location allows for quick connections, further enhanced by terminal placement. Passengers don’t have to worry about customs or transit when moving from one flight to the next. In addition, the company operates a single-type fleet, further controlling costs by limiting maintenance hassles, training needs, and parts inventory.

Copa Holdings Accelerates Growth in Q1 2026

Forget the million-dollar nest egg (Ad)

Nearly 2 in 3 Americans fear running out of money more than death - and chasing a $1.5 million nest egg isn't helping.

Tim Plaehn has spent decades helping people build retirement income, and he says the monthly income goal is the only number that matters. His approach could potentially reach that goal with 10x less capital - using a single stock you can buy with one click.

Watch the short presentation to see how this retirement income strategy worksCopa Holdings had a strong Q1, with revenue growing 17% to just over $1 billion, underscoring its strength. The top line exceeded MarketBeat’s consensus estimate by a wide margin, accelerating from the prior quarter and year due to increases in capacity and demand. The bullish detail is that passenger traffic increased 15% on a 14% increase in capacity, helping drive margin strength and further supported by improved revenue per mile.

Margin news is also strong. The company widened its operating and net margins despite higher costs, particularly fuel costs. GAAP earnings grew at an accelerated 20.5% pace, exceeding the consensus estimate by 73 cents, or nearly 1,650 basis points (bps). Looking ahead, the company issued a cautious Q2 forecast, citing fuel cost headwinds, but remained positive for the year, forecasting 17% revenue growth.

Bullish Cash Flow and Capital Return Outlook Drive CPA Price Action

Copa Holdings' highly efficient business enables healthy cash flow and capital returns, including dividends and share buybacks. Dividends are approximately 40% of earnings and remain reliable in 2026, yielding approximately 4.5% with shares trading near historically high levels.

Distribution increases are expected given the revenue and growth outlook, and they will likely continue at a robust double-digit pace in the coming years. Share buybacks are less aggressive but still provide value, reducing the share count by an average of 0.3% over the trailing 12 months (TTM).

Institutional activity is mixed, with the balance bullish but relatively flat on a trailing 12-month basis as of mid-year. However, institutions provide solid support, owning about 70% of the shares, and the analysts are more bullish.

MarketBeat reveals increasing coverage, firming sentiment, and rising price targets, with a consensus Buy rating and a forecast for fresh all-time highs. Short interest does not appear to be an issue. It is slightly elevated at around 4% but not alarming, and is more likely linked to hedging activity than outright bearish behavior.

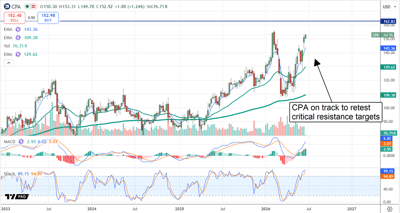

Copa Holdings Advances: Approaches Critical Threshold

Copa Holdings’ price action is bullish in Q2. The market is advancing and on track to test resistance at the existing all-time high. Bullish signals in the MACD and stochastic suggest the retest will come soon, potentially by year’s end, and new highs are possible. Setting new highs would be significant, as they would be the first fresh highs in over a decade, opening the door to a much larger move.

In this scenario, the base case is worth the dollar value of the existing trading range, which runs from $120. A move to $280 is possible, assuming a fresh high is set. If not, CPA shares may remain range-bound indefinitely, but that is not expected given the growth and capital return outlook.

Copa Holdings' business is supported by robust demand in a major emerging market region. Latin America is a leading growth pillar internationally, driven by industrialization and middle-class expansion, which are fueling demand for business and leisure travel. Consistent capital returns are expected over time. The biggest risk for Copa is geopolitical. Not only can conflicts outside the region impair travel demand, but internal issues could disrupt business. Numerous international agreements enable easy, free-flowing traffic among many of the nations served.

Copa Holdings’ balance sheet is not among its risks. The company maintains low leverage and ample cash, which equates to 40% of TTM revenue as of the end of Q1. The likely outcome is that Copa Holdings will continue to execute its strategy, investing in growth while returning capital to investors.

Beyond the AI Trade: 3 Defensive Stocks Built for Stability

Submitted by Thomas Hughes. Article Posted: 6/20/2026.

Key Points

- Tech stocks are the hot trade, but with crowded markets come volatility: here are three ways to reduce portfolio risk.

- Qualities to look for include stable business demand and reliable dividends.

- Smart money, as indicated by institutional trends, values diversification and the cash flow from safe-haven investments.

- Special Report: Forget SpaceX. Buy the company Musk can't replace.

AI stocks are the hot trade in 2026 and may continue to dominate markets. However, figuring out which AI stock will post the next big move is difficult, which is why diversification matters. Diversification can help protect portfolios from unnecessary volatility and risk, delivering steadier, if slower, returns while investors wait for those higher-risk tech stocks to appreciate. Defensive stocks often share a few traits, including stable demand, reliable dividend payments, and lower-than-average beta.

Beta is a widely misunderstood metric. It measures a stock’s volatility relative to a benchmark, typically the S&P 500, rather than the expected volatility of the underlying issue. Low-beta stocks are not immune to volatility, but they have historically been less sensitive to broad market moves. Their price action tends to be less tied to macroeconomic swings than the average stock because of income stability and capital returns.

UnitedHealth Is Set Up for Sustainable Price Recovery

I paid $5,000 to hear Elon say this (Ad)

One investor paid $5,000 to be in a private room with Elon Musk in Los Angeles - and what he heard confirmed a conviction 15 years in the making.

Musk is launching a project 27 years in the making that could be his biggest move yet. One analyst believes there is a single stock positioned to benefit most - and he is giving away the name for free.

Get the free stock pick tied to Elon's most ambitious projectUnitedHealth (NYSE: UNH) has struggled over the past year with an executive shakeup, legal woes, and margin pressure. However, the company has navigated those headwinds well, putting itself in position to resume growth in the coming quarters, accelerate it, and improve profitability. That supports a healthy capital return outlook, which includes dividends and share buybacks. The dividend yields more than 2.25% annualized as of mid-June and is expected to grow over time.

UNH is on track to be included in the Dividend Champions index, has increased its distribution at a double-digit compound annual growth rate over the past few years, and pays out approximately 50% of its earnings. Share buybacks are also substantial, having reduced the share count by an average of nearly 1% as of Q1 2026.

UNH’s beta is very low at 0.64 over the trailing three years. Factors contributing to the low beta include the company's predictable cash flow, visible catalysts, and capital returns. Its shareholder base also includes a high percentage of long-term, buy-and-hold investors.

Despite recent woes, analysts have maintained a Moderate Buy consensus for UNH stock. The story in mid-2026 is that price targets are rising again, signaling a reversal in this market. Institutional activity is also robust, with institutions owning approximately 88% of the shares and accumulating for seven consecutive quarters.

Brookfield Corporation: The Crown Jewel of Real Asset Investing

Brookfield Corporation (NYSE: BN) is the crown jewel of real asset investing and the world’s largest alternative investment corporation. Real assets are tangible investments such as commodities, natural resources, real estate, and infrastructure. They are an asset class in their own right, attractive for their intrinsic value, inflation resistance, and cash-generating qualities. The company operates in three segments, providing exposure to wealth management, insurance services, and direct asset ownership.

Among Brookfield’s attractions are its cash-generating qualities and capital returns. The dividend is barely more than a token at a 0.6% yield, but it's complemented by share buybacks. The latest authorization is worth up to 10% of the share count, with trailing-12-month activity reducing the count by approximately 0.65% as of Q1.

Brookfield is not a low-beta stock, as it is exposed to commodity price swings and geopolitical risks. However, it is viewed as a safe haven because of its tangible assets, inflation-linked cash flow, and substantial fee-based management business. That combination provides steady, predictable cash flow, enabling business growth, financial strength, and capital return.

American Electric Power: Monopolizing Cash Flow and Capital Return Safety

Utility companies are traditional safe-haven plays with heavily regulated, entrenched businesses. Operators like American Electric Power (NYSE: AEP) provide stable, steady income, reliable yields, and growth opportunities. Not only is the U.S. power grid old and ailing, in need of updating, but demand is growing and expected to remain strong in the coming years. Data centers are only part of the story, as growth in the household and business sectors is also at play.

American Electric Power provides a strong dividend, yielding nearly 3% as of late Q2 2026. The payout ratio is a bit high, at over 60%, but that is only when compared with average companies. Utilities such as AEP, with highly visible and relatively unimpeded cash flows, tend to sustain a larger portion of earnings in payouts. Regulation means rising costs can be offset by higher prices, which is a catalyst in the industry today.

AEP’s stock beta is approximately 0.53, reflecting price action that is only about half as volatile as the average stock. Fundamentally, AEP is in an uptrend, supported by rising demand and plans to expand capacity, which have analysts buzzing. In their view, datacenter demand changes the story from humdrum utility to a high-growth story with legs.

This message is a sponsored email from Investors Alley, a third-party advertiser of MarketBeat. Why was I sent this message?.

All information contained herein is copyright 2026, Magnifi Communities LLC.

If you need help with your newsletter, feel free to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. United States of America..

No comments:

Post a Comment