This is the gold setup I’ve waited my entire career for…

And after 31 years in this market, I don’t say that lightly.

I’ve walked the mine sites. Met the management teams. Studied the drill results. And found opportunities before the crowd caught on…

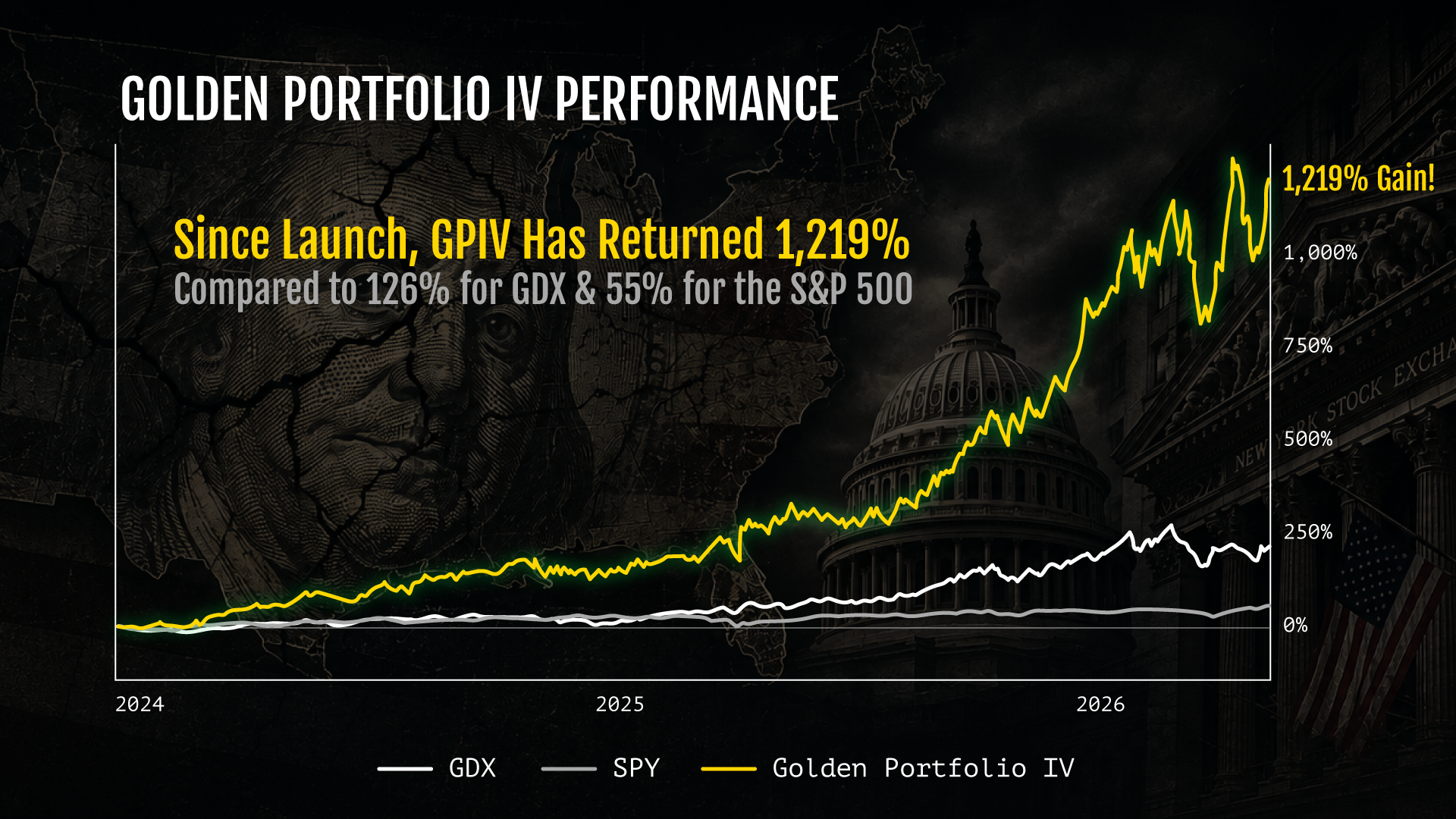

That’s how my gold portfolio climbed more than 1,200% in the last two years alone…

Including individual gains of 1,023% in G2 Goldfields… 741% in Highlander Silver… 538% in Reunion Gold… 416% in Orogen Royalties… and 126% in Newmont.

Enough to turn $100,000 into more than $1.3 million.

But I believe the opportunity in front of us now could be even bigger.

Because this isn’t just another gold rally.

It’s a monetary shift.

And for anyone who moves before the crowd catches on…

It could open the door to one of the biggest profit opportunities I’ve ever seen.

And the clue came from a place most investors would never think to look:

Riyadh.

In June 2024, a little-known 1970s arrangement between Washington and Saudi Arabia quietly expired.

Most analysts ignored it.

I couldn’t.

Because I believe it could mark the beginning of a major shift away from the dollar system…

And toward hard assets like gold.

Today, the instability in the Middle East is accelerating this exodus away from the U.S. dollar.

Which is why I’ve identified one tiny company I believe could benefit most.

If I’m right, this stock could double, triple… or even 10X your money.

A $5,000 stake could become $10,000… $15,000… even $50,000.

A $10,000 stake could become $20,000… $30,000… even $100,000.

But after 31 years in this market, this is exactly the kind of rare setup I wait for.

Click here now to watch my urgent briefing.

Regards,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio

P.S. This is a fast moving story that’s why I’m urging you to watch this briefing today. Because if I’m right, this tiny company could double, triple… or even 10X your money as this monetary shift unfolds. Go here now to get the details.

CarMax In Reverse? Why You Should Buy Now Before the Big Catalysts Emerge

Author: Thomas Hughes. First Published: 6/18/2026.

Key Points

- CarMax's stock price reversal is driven by a CEO change and operational improvements gaining traction.

- Analysts' trends are shifting, with activity stabilizing the consensus price target, setting the stage for bullish catalysts to emerge.

- Subsequent results, an investor day strategy update, and capacity for capital returns can trigger more aggressive accumulation in this market.

- Special Report: Everyone wanted SpaceX. Smart money wants this.

CarMax (NYSE: KMX) entered a market reversal earlier this year as it transitioned to a new CEO and activist investors took positions. The story now is that Keith Barr’s four-pillar strategy to increase volume, improve digital sales, add value on each transaction, and drive efficiency is gaining traction.

The question is whether CarMax can preserve its cost savings and return to profitable growth in the coming quarters, and the early signs are encouraging. In this environment, CarMax remains in the middle of an evolving catalyst, with the stronger signal—sustained operational improvement—still to come.

CarMax Outperforms in Q1, First Report With New Ceo

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidCarMax faced headwinds in Q1 fiscal year 2027 (FY2027), including uneven consumer demand and affordability pressure, but performed well, with unit volume increasing by 3.3% across the system.

Revenue grew by 6% to just over $8 billion, outperforming expectations by more than 780 basis points. Segmentally, wholesalers did the heavy lifting, with units up 8% compared with a basically flat retail side.

Lower relative pricing aided the strength and is reflected in the margin. The company managed to reduce selling, general and administrative (SG&A) expenses and improve efficiency on a per-unit basis, but gross margin impairment offset those gains. The takeaway is that gross profit declined by nearly 5%, net margin contracted by approximately 50 basis points despite an improvement in SG&A, and GAAP earnings declined.

The offset is that earnings per share (EPS) of $1.31 outpaced consensus by a wide 34-cent margin, providing sufficient cash flow to sustain operations and maintain balance sheet quality. CarMax's balance sheet carries debt, but it did not raise any red flags for investors.

The company does not provide specific guidance on operational metrics, but it did offer color on what to expect this year. As it stands, the focus is on improving sales and customer satisfaction, which will put pressure on margins. That trade-off is important for investors to watch. Lower asking prices can help rebuild unit volume, while continued investment in digital services may weigh on profitability until those efficiencies scale.

Among the critical Q1 takeaways, however, are the 84% of retail unit sales supported by digital capabilities and 14% online retail sales, with digital channels central to reducing time to close, improving customer outcomes, and supporting longer-term operating efficiency.

Analyst Sentiment Trends Key to CarMax’s Stock Price Outlook

Analyst sentiment is central to CarMax’s 2025 stock price decline and 2026 rebound.

After price target cuts and weaker coverage weighed on KMX in 2025, the tone in 2026 has shifted toward cautious optimism as investors evaluate the CEO transition and early signs of operational improvement.

Analyst activity since February 2026 has included initiations, reaffirmed targets, and, more recently, price target increases that have helped stabilize the consensus estimate.

The consensus price target is around $42, below the current share price but aligned with the technical price floor put in place last year, and is likely to advance amid operational improvements and strengthen the expected catalyst.

Institutional trends look more bullish despite mixed activity over the trailing 12-month period. Selling outweighed buying in parts of 2025, but activity in the first half of 2026 suggests renewed accumulation. More importantly, the periods of accumulation and distribution align with CarMax’s price action, revealing group buying on dips and market support at the lower end of its trading range.

The likely outcome is that KMX's downside is limited, and institutional support will strengthen in subsequent quarters.

CarMax Catalysts: There Is More Than One Coming Down the Pipe

CarMax has several catalysts coming down the pike, centered on its upcoming earnings reports. Those reports are expected to show improvements in cash flow and future profitability. Among the catalysts is the capacity for capital return, which centers on share buybacks.

CarMax paused share repurchases in the latest quarter, but prior buybacks have still reduced the company’s share count over the past year. A resumption of repurchases could become a bullish catalyst if earnings stabilize. Management is also expected to provide more details on its turnaround strategy later this year.

Chart price action is not bullish following the release. The market for KMX stock is down more than 5% and may continue to decline in the near term. The caveat is that this market appears to be in the midst of a Double-Bottom Reversal, and the mid-June pullback is testing critical support.

Assuming support holds, KMX shares could advance this summer, potentially reaching $70 by early fall. If not, a move to retest recent lows near $37.50 is probable—lower lows are not expected this year.

The Quantum Bubble Is Real Enough to Take Seriously

Author: Nathan Reiff. First Published: 6/30/2026.

Key Points

- Quantum computing stocks have rallied sharply, but investors still need to weigh valuations against current revenue, profitability, commercial demand and cash burn.

- D-Wave and Rigetti both trade at extremely high sales multiples, with Rigetti’s revenue decline making future contract wins especially important.

- IonQ shows stronger revenue growth and commercial traction, but high R&D spending and potential dilution remain key risks across the sector.

- Special Report: Everyone wanted SpaceX. Smart money wants this.

As with the AI industry, investors often dismiss the quantum computing sector as a "bubble." In both cases, however, it is important to understand what that characterization really means. Quantum technology, like AI, is undoubtedly real and rapidly developing—even if the eventual end goals and use cases are not always clear to those outside the space. As a result, concerns about a potential bubble have less to do with the technology itself and more to do with whether current market valuations for quantum companies have risen too far, too fast, relative to the stage of the underlying technology.

A balanced approach to evaluating a potential quantum bubble must consider valuations relative to revenue, profitability, commercial demand, cash runway, and external threats.

The Valuation Growth Issue

ALERT: Drop these 5 stocks before the market opens tomorrow! (Ad)

The Wall Street Journal is already raising the alarm about a potential market crash, and Weiss Ratings research points to the first half of 2026 as a particularly rough stretch for certain holdings.

Some of America's most popular stocks could take serious damage as a radical market shift plays out. Analysts at Weiss Ratings have identified five names you may want to remove from your portfolio before this unfolds.

If any of these are in your portfolio, now is the time to review your positions.

See the 5 stocks to avoidMany pure-play quantum computing companies have seen rapid share price appreciation in recent years: D-Wave Quantum Inc. (NYSE: QBTS) is up 68% over the last year, for example, while Rigetti Computing Inc. (NASDAQ: RGTI) has climbed about 65% during that period.

Investors will want to see revenue expanding in a way that supports those valuation gains. In D-Wave's case, full-year 2025 revenue increased 179% year over year (YOY), while Rigetti's full-year 2025 revenue declined from the prior year. Despite D-Wave's impressive growth, revenue remained low in absolute terms, with the company reporting around $25 million for all of 2025.

To monitor how valuation and revenue line up, investors should keep an eye on metrics like the price-to-sales ratio. Both companies recently traded at extremely high sales multiples, with D-Wave above 700 times sales and Rigetti even higher.

That gives investors reason to question whether those stock prices have moved too far ahead of current revenue.

Rigetti underscores why that concern is not just theoretical. Unlike D-Wave, its 2025 revenue declined from the prior year, making future contract wins and revenue conversion especially important for the stock.

Profitability and Demand Concerns

It is not just sales that determine the viability of quantum computing firms. Profitability is essential as well. Many companies in this space still share common traits, including negative operating margins and free cash flow, high spending on R&D, and continued reliance on external capital. While that is typical for companies in the early stages of development, investors will want to know whether valuations are already pricing in profit levels that are still many years away.

IonQ is a good example, particularly because it has one of the largest revenue bases of any company in this industry (in Q1 2026, the company reported almost $65 million in sales, up 755% YOY). Along with strong sales growth, IonQ also has an advantage in that it is quickly building commercial traction—something not all quantum firms have managed so far.

Even so, with GAAP R&D costs more than tripling YOY to almost $126 million in Q1 2026, IonQ faces a major hurdle on the path to profitability. Like many other pure-play quantum names, it will need to find additional sources of funding in order to keep developing its technology.

A Bright Spot: Cash Reserves

While cash run rates remain high, one bright spot for some pure-play quantum companies is their cash reserves. IonQ ended Q1 2026 with $3.1 billion in cash, for instance, while D-Wave has been able to use its cash position to make an aggressive acquisition earlier in the year. This suggests that these companies have reasonable runways and are not in immediate danger of collapse. Investors will still want to see signs that they can generate enough free cash flow over time to support their expenses, though.

Another question for investors is whether these companies are building cash reserves in a way that dilutes shareholders. The industry has become known for capital raises through the sale of additional shares, a move that can provide near-term cash but may also dampen investor enthusiasm and signal longer-term challenges.

The Looming External Threat

A final factor for investors to watch is the external threat posed by larger tech firms entering the quantum computing corner of the sector. Companies like D-Wave and Rigetti are tiny compared with rivals that have growing quantum initiatives, such as Intel Corp. (NASDAQ: INTC) and IBM Corp. (NYSE: IBM), both of which have recently signaled plans to double down on their quantum operations.

Interest from legacy tech companies is likely to benefit quantum technology as a whole. However, it may be harmful, or even devastating, for smaller firms already facing the pressures described above. All of this adds to the risk profile of these companies, which investors must keep in mind.

This email message is a paid sponsorship sent on behalf of Golden Portfolio, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you have questions about your newsletter, please contact MarketBeat's South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place, Sixth Floor, Sioux Falls, South Dakota 57103. U.S.A..

No comments:

Post a Comment