Hello - Your free report is attached: These 7 Stocks Will Be Magnificent in 2026.

Inside, you'll find seven companies positioned for sustained growth, along with the key metrics that separate long-term winners from short-term momentum plays.

Download your free report here. (PDF)

To your investing success,

Matthew Paulson

MarketBeat

P.S. If you need help accessing this report or using MarketBeat in general, just drop us a note at contact@marketbeat.com. Our South Dakota–based support team is always happy to assist.

Exclusive Content from MarketBeat

MongoDB's AI Advantage Is Starting to Show Up in ResultsAuthor: Thomas Hughes. Published: 5/30/2026.

Key Points

- MongoDB is on track to accelerate its rebound after accelerated results and guidance.

- Its non-structured database is well-suited to agentic workloads, which underpin results.

- Risks include intense competition from leading players like Oracle.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

SQL has long been the standard for database queries, but it was built for a structured world—and AI does not live in one. MongoDB (NASDAQ: MDB) recognized that early. Its document-based architecture supports hybrid searches across structured and unstructured data at the same time, enabling unified memory, flexible integrations, and the kind of real-time contextual awareness modern AI applications demand.

Porter Stansberry, founder of one of the largest financial research firms in the world, says he's breaking the biggest story of his 26-year career - an economic shift not seen since 1776.

From the government taking stakes in Intel, Lithium Americas, and MP Materials, to sweeping political changes reshaping the economy, Stansberry argues a rare 'New 1776 Moment' is already underway. One Nobel Prize winner calls it a dividing line for all of society.

His presentation covers the stocks to buy, the stocks to sell, and three money moves to position yourself on the right side of this shift. Watch Porter Stansberry's full briefing and learn how to prepare now

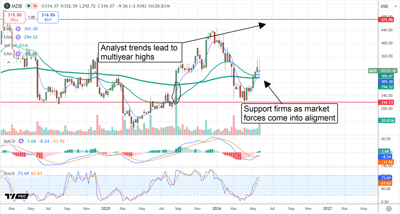

That foundational advantage took time to translate into business results, but as the latest fiscal earnings report shows, the traction is now undeniable—and the AI flywheel MongoDB has built looks poised to keep spinning well into the future. MongoDB Accelerates in Q1: Strong Guidance May Still Be ConservativeMongoDB had a strong quarter, with revenue of $687.62 million, up more than 25% from last year. That marked an acceleration from the prior year, came in 350 basis points better than expected, and was supported by strong guidance. The company forecasts growth to slow next quarter to about 23% at the midpoint, roughly flat year over year (YOY), but there is still significant room for outperformance. MongoDB's Q1 results were underpinned by strength in the Atlas platform, subscriptions, and services, with growth across all regions and client groups. Total clients grew by 18.5%, while Atlas clients, the company's enterprise-quality deployment, management, and developer platform, outpaced that figure at 18.9%. Large clients contributing more than $100,000 in annual recurring revenue were also solid, rising 15% and expected to remain healthy in the coming quarters. Margin news was also encouraging. The company widened its GAAP gross margin, maintained a high adjusted gross margin, and improved profitability across the board. GAAP operating losses narrowed, adjusted profits grew by 41%, net profits rose by 30%, cash flow nearly doubled, and free cash flow improved by 87%. This left the balance sheet virtually unchanged after the first quarter despite acquisitions, investments, and capital returns. Capital returns are not aggressive at this time, but they are offsetting share-based compensation and should increase over time. Factors supporting the outlook for outperformance in upcoming quarters include remaining performance obligation (RPO) and current RPO. RPO represents the value of contracted but unrecognized revenue, and it grew by 88%. CRPO, a measure of contracted revenue expected to be recognized in the next 12 months, also increased substantially, by approximately 70%, and is likely to keep rising in the current and subsequent quarters. Analysts Are Bullish—And the Numbers Back Them UpThe analyst response following the release was overwhelmingly bullish, with numerous price target increases within the first day. Takeaways from the chatter include exceptional growth across both Atlas and Enterprise Advanced platforms, multicloud strength, momentum in agentic workloads, and improved guidance. The fresh revisions put MDB at the high end of the analyst price target range, strengthening conviction in the consensus forecast. Consensus would put this stock near $385, a multimonth high, while the high end adds more than 20% to that level. The likely outcome is that MDB continues to gain momentum, delivers solid results in upcoming quarters, and analysts sustain the bullish trend, driving the stock to a multiyear high. MongoDB’s valuation remains one of the main risks for investors. Trading at more than 50X the current year's earnings outlook and 30X the 2030 consensus, the stock is not cheap, and much of the growth may already be priced in. Execution will be key in this environment, but that does not appear to be an issue at this time. As it stands, the company is outperforming consensus estimates and lifting guidance, suggesting the forward outlook may be too cautious. MongoDB Faces RisksAnother risk is the intense competition the company faces. While SQL is the dominant database format globally, hyperscalers across the board have developed, or are rolling out, their own NoSQL databases. Oracle (NASDAQ: ORCL) is a leading competitor and an entrenched player in the AI hyperscale ecosystem. The caveat is that this market is still in its infancy, and there is room for numerous players to benefit. The global database industry is valued at approximately $200 billion and is forecast to grow at a modest double-digit CAGR for the foreseeable future. Stock price action was mixed following the release. The market advanced, but gains were capped near short-term highs, suggesting a sharp rebound may not be imminent. However, the stock remains in consolidation above a cluster of moving averages, with institutional activity showing accumulation.

The likely outcome is that MDB continues to consolidate at late May levels, with the potential to resume advancing by mid-summer. Critical factors include the spike in volume that accompanied the earnings-week price action, a sign of strong support and market conviction, and the 90% institutional interest. |

No comments:

Post a Comment