What if you could throw out all your charts… moving averages… stochastics… bollinger bands.. candlestick patterns…

And actually have a shot at A BETTER WIN RATE?

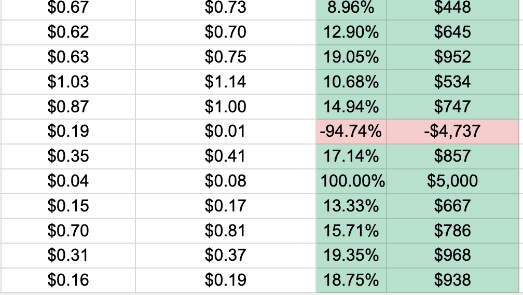

That's what veteran trader Alex Reid did…

And over more than 100 vetted real money trades, he hit an 86% win rate…

With 11 winners out of the last 12 trades.

*Last live closed trades from October 30th to November 6th, 1 day average hold time. There were also smaller winners, and as you can see, losing trades. We can't promise future gains or against losses.

Now, we certainly can't make reckless guarantees when it comes to trading…

But Alex has been on fire with this new strategy…

And even though he didn't use any of the common tools that most traders use…

We develop tools and strategies to the best of our ability but no one can guarantee the future. There is always a risk of loss when trading. Past performance is not indicative of future results. What you will see today are some of the best examples from the public trade research service that utilizes this underlying method. From January 2024 through November 2025 the win rate was 86% with a 40.9% average winner and 23.3% average net return of winners and losers over a 1 day average hold time. There were bigger winners, there were smaller winners and there were losers. Trade at your own risk.

Today's editorial pick for you

Chewy Earnings: Good Report, But Is the Stock's Big Move Already Behind It?

Posted On Mar 26, 2026 by Chris Markoch

Chewy (NYSE: CHWY) stock surged more than 13% on March 25 after the online pet retailer delivered its fiscal fourth-quarter and full-year 2025 earnings. The report showed a company quietly building something durable, even if the headline numbers don’t exactly set the pulse racing. For investors who had been circling CHWY ahead of this “prove it” moment, the Chewy earnings report delivered enough to justify the pre-report positioning. The harder question now is what comes next.

Table of Contents

Q4 net sales came in at $3.26 billion, up 8.1% year over year — a consistent result that extended a full year of steady mid-to-high single-digit quarterly growth. For the full fiscal year, Chewy posted net sales of $12.6 billion, up 8.3% year over year, while active customers grew to 21.3 million with 813,000 net adds. Net sales per active customer rose to $591.

Those aren’t blockbuster numbers, but they reflect steady, consistent execution. The headline that seemed to tip sentiment bullish was a record $232 million in free cash flow for the quarter, capping a full year that generated $562 million in free cash flow with a cash balance of $879 million at year-end.

The story here isn’t about explosive growth. It’s about a company that has quietly matured into a cash-generating machine with a deeply loyal customer base. Whether that’s enough to sustain a meaningful rally, or whether smart money already got what it came for, is the defining question for CHWY going forward.

Solid Fundamentals, But Growth Stays in Single Digits

The numbers Chewy delivered were good, not great, and that’s actually the point. Eight percent revenue growth is respectable for a company operating at this scale, and the consistency across all four quarters of fiscal 2025 tells a story of a business that has found its rhythm. Investors who were bracing for a stumble didn’t get one.

The engine underneath that top-line growth is Autoship, Chewy’s subscription-like recurring revenue program. Full-year Autoship customer sales reached $10.5 billion, up 14% year over year, and represented 84% of net sales in Q4 alone. That is an extraordinary stickiness metric. Pet owners who sign up for Autoship tend to stay, and that predictable revenue stream is the bedrock of the bull case.

Margin expansion continued as well. Full-year gross margin reached 29.8%, up from 29.2% in fiscal 2024, and adjusted EBITDA grew to $719 million for the year, a 5.7% margin that represents 90 basis points of improvement year over year. Q4 adjusted EBITDA came in at $162 million at a 5.0% margin, a seasonal step-down from the stronger middle quarters but still meaningfully ahead of where the company was a year ago. The margin trajectory is moving in the right direction, even if the pace is measured rather than dramatic.

Technical Picture: Can the Stock Hold Its Ground?

The chart tells a sobering story when you zoom out. CHWY spent most of the past nine months in a grinding downtrend, shedding nearly half its value from the mid-$40s to fresh lows near $23 before this morning’s pop. The 50-day simple moving average, currently around $27.34, served as a ceiling for much of that decline. Now, with the stock closing around $26.51, the question is whether today’s surge can flip that resistance line into support.

A clean consolidation above the 50-day SMA would be a technically constructive development — the kind of base that, if it holds, could attract fresh institutional buying and set up a higher trajectory heading into fiscal 2026.

The MACD remains in negative territory, suggesting the momentum shift is still in early innings. Volume on today’s move, nearly 18 million shares, was elevated, which adds credibility to the reversal. But one day does not a trend make. Bulls need to see follow-through and a stock that can absorb profit-taking from those who bought in anticipation of the report.

What Could Actually Turn the Bulls Loose?

For fiscal 2026, Chewy guided net sales of $13.60 to $13.75 billion, implying roughly 8% growth, along with an adjusted EBITDA margin of 6.6% to 6.8% — another step of meaningful expansion. For Q1 2026 specifically, management guided net sales of $3.33 to $3.36 billion with adjusted diluted EPS of $0.40 to $0.45. That’s a competent forecast, but it’s essentially a “run it back” script. There are no obvious catalysts to dramatically change the growth profile, unless a few things start to click.

The Autoship engine will need to keep humming. Any acceleration in net sales per active customer beyond the current $591 trajectory would signal that existing customers are deepening their relationship with the platform, which is the highest-quality growth Chewy can generate. Gross margin expansion is also a lever worth watching. If the company can push toward 30.5% or better through mix shift and operational efficiency, the EBITDA flow-through could surprise to the upside and give the stock a fresh catalyst beyond the current guidance range.

A Company and a Stock Are Different

Chewy is a well-run company with genuinely loyal customers, a strong subscription model, and improving cash generation. The fiscal 2025 results validated that narrative. But the stock ran hard into earnings, and the guidance, while respectable, isn’t the kind of upside surprise that typically sustains a post-earnings rally for weeks. The most likely near-term path is a test of whether CHWY can consolidate around the 50-day moving average and build a base.

Long-term investors who believe in the pet-economy thesis have a reasonable entry point. Short-term traders may find they were right about the report and early about the exit. The pet business is sticky. The question is whether the stock can be too.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

No comments:

Post a Comment