"KMB has had a history of strength for the past 53 years." Karim Rahemtulla, Co-Founder, Monument Traders Alliance Publisher's Note: We're just two days away. On Wednesday, March 4, at 1 p.m. ET, The Oxford Club's Chief Income Strategist Marc Lichtenfeld will be showing traders a major catalyst that could lead to a once-in-a-generation run for gold. The event is completely free. Click here to sign up today. - Stephen Prior, Publisher

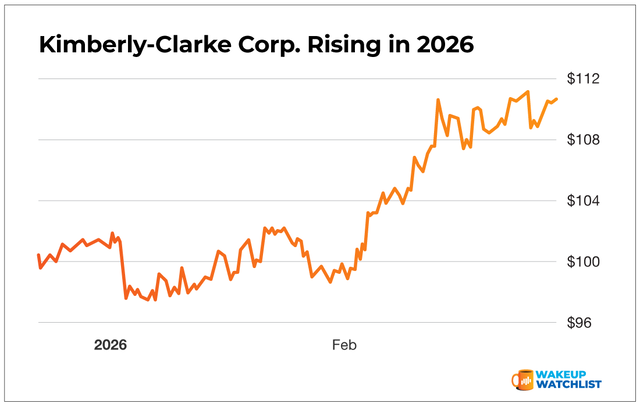

We've been talking a lot about cash inflow rotation in the biotech sector over the past few weeks. But there's also another sector worth adding to your watchlist right now. Consumer staples. This sector is seeing strong cash inflows in 2026 - and one name in particular stands out. Kimberly Clarke-Corp (KMB). You might know the brand - Huggies, Kleenex, Cottonelle, Scott. These are the products people buy whether the economy is booming or busting. KMB peaked at an all-time high in March 2025, and has since pulled back. That pullback is creating a buy opportunity right now. I've been trading KMB profitably in both The War Room and Monument Trend Advisory this year. Here's what has me excited about it... First, strong insider buying. In early February, Director Todd Maclin bought 10,000 shares worth $1,041,500. When a corporate insider writes a million-dollar check, it means they think the price is going up. Second, it has a super low valuation. KMB has pulled back to levels that look cheap relative to its history - but it's not a broken business. Consumers buy toilet paper and tissues in both bull and bear markets, so the return potential is strong. And third, KMB is a certified "dividend king." It has raised its dividend for 53 consecutive years - through recessions, rate hikes and market crashes. That kind of consistency means KMB prioritizes shareholders. As you'll see above, KMB is up 9% in 2026, and I believe it's still a bargain at its current price. |

No comments:

Post a Comment