Let's say gold is $2,000/oz and it costs a gold miner only $1,000/oz to mine and process that gold. That miner's margin is 50%, well above where we are at now at $1,472/oz AISC.

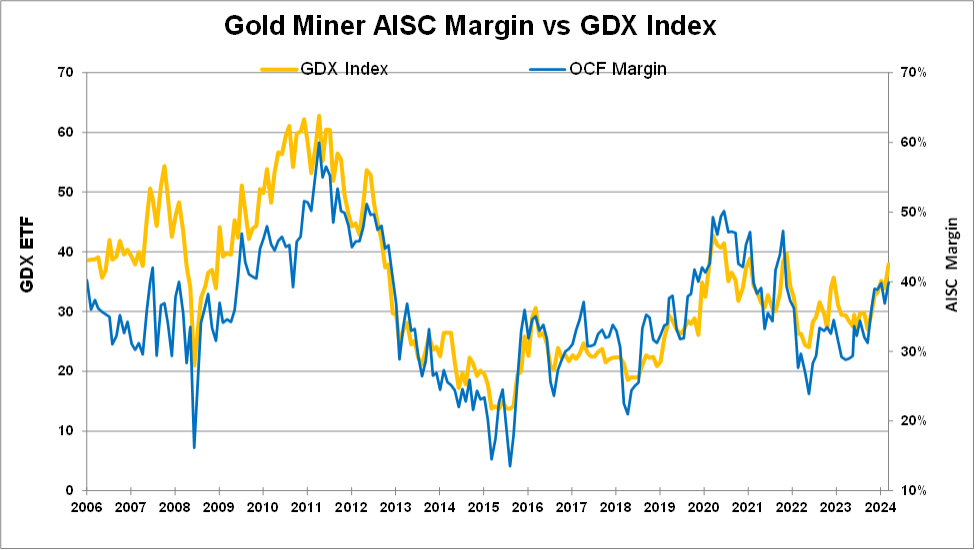

Note how closely the average miners' margin and the average gold miner, represented by the HUI Index, track.

The GDX and margins peaked out in 2011 when gold was at $1,836/oz and costs were $540/oz resulting in a 71% margin. Now the gold price is trading for about $2,500/oz and AISC is $1,472/oz resulting in a 41% margin.

At peak 71% margins the GDX was trading for $60 per share. Now, at current 41% margins, the GDX is trading for $37 per share, a decline of 38%.

We have no doubt margins will one day match the 71% margins in 2011 when the gold price spikes higher.

But what's the upside for the miners?

The GDX will likely climb back to $63 per share, only a 1.7X gain. Then as costs climb, decreasing margins, the GDX will decline in lockstep.

I can show you a better way. A small group of gold companies with no exposure to costs, only leveraged to the gold price.

Since costs are locked in, when gold climbs, margins increase indefinitely. These companies provide accretive growth not tied to the cyclical nature of the mining industry.

That's it for today…

Tomorrow, I'll cover what I believe is the most important factor when analyzing mining stocks.

Best,

Garrett Goggin, CFA

Founder, Golden Portfolio

P.S. Your two FREE recommendations will be sent to your inbox after this 5-Part Masterclass. I've personally picked two of my favorites to share with you. One from Golden Portfolio and one from Golden Portfolio 10X. Keep an eye on your inbox.

No comments:

Post a Comment