Dear Reader,

The same AI tech that predicts heart failure and grid blackouts... has now learned to forecast U.S. stock prices, to the cent, days in advance.

Here is how to try it right now for free.

I'm writing to announce my firm's breakthrough new system: a new form of financial AI... that can forecast the price of 2,384 U.S. stocks, to the penny, up to 21 days in advance.

If you had access to this AI over the last few years... based on its average winning recommendation... you could have tripled your money every single year.

To make this, it took $22 million across our firm's history... plus the genius of a former Air Force nuclear missile coder.

But it's finally live.

And you don't have to sign any forms or make ANY long-term commitments to see it in action for yourself.

No email required. No credit card required. We're offering a completely free, no-strings-attached demo of this stock forecasting AI, right now.

Click here to learn more – and access your free demonstration.

Regards,

Keith Kaplan

CEO, TradeSmith

Dividend Increases: From Over 10% Yields to Over 10% Dividend Growth

By Leo Miller. Article Posted: 6/24/2026.

Key Points

- A mortgage REIT with a yield already well above 10% just issued a solid boost to its quarterly payment.

- A consumer staples stock putting up large returns just lifted its dividend by 14%, staying with its multi-year trend of large increases.

- After appointing a new CEO, this large retailer is seeing a resurgence in its shares while also providing a strong dividend yield.

- Special Report: The company SpaceX cannot operate without

Several stocks spanning the range from high dividend yields to rapid dividend growth have just added more juice to their payouts. These stocks offer yields that climb above 13% at the high end, while also delivering recent dividend increases of up to 14%. That gives investors multiple ways to think about the yield-versus-growth tradeoff.

Annaly: High-Yield Mortgage REIT With Notable Risks

Annaly Capital Management (NYSE: NLY) is a real estate investment trust (REIT) with a very high dividend yield. The company is specifically involved in managing mortgage-backed securities (MBS) and other types of debt.

A letter from Shannon Stansberry (Ad)

Porter Stansberry nearly canceled the entire project. When he first saw the claimed returns - only one down year in nearly two decades and total gains of almost 2,000% - his immediate reaction was disbelief.

It took a trusted friend's personal vouching for Emmet Savage and a face-to-face trip to Ireland to change his mind. The full documentary, Investigating Project Prophet, is now live.

Watch the full story and see the verified track record for yourselfAs a mortgage REIT, the company’s value proposition rests on its ability to identify and generate returns on MBSs, which then flow to its bottom line. After the company’s latest dividend increase of 7%, Annaly now has an indicated dividend yield near 13.5%. The company’s next dividend is payable on July 31 to shareholders of record as of June 30.

However, one important risk to understand is Annaly’s use of leverage to generate returns, which increases both upside and downside volatility. Still, Annaly argues that it uses leverage more effectively than others in its industry.

Specifically, the firm notes that its economic return per unit of leverage is 2%, or 30% higher than that of the average mortgage REIT.

In other words, the company has used less leverage than its competitors to generate the same gain on its underlying investments. Annaly has executed its strategy well, delivering a total return of more than 40% since the start of 2025. Approximately half of that return has come from dividends. Overall, Annaly’s large dividend yield is appealing, but leverage risk is something investors must take into account.

Casey’s: Expanding Dividend Rapidly, Rising Shares Weigh on Yield

Casey’s General Stores (NASDAQ: CASY) may not be in tech or artificial intelligence, but this consumer staples stock has been delivering big returns nonetheless. After rising 40% in 2025, Casey’s has returned approximately 50% in 2026. The convenience store and gas station chain has made a name for itself with its in-house food, best known for its pizza.

The company has consistently outperformed analyst expectations, with its latest earnings report serving as another reminder of that strength. Sales grew 14.5% year over year (YOY) to $4.57 billion, solidly beating estimates, while earnings per share (EPS) soared 66% to $4.37. This allowed Casey’s to crush expectations of $3.31 by more than $1, sending shares up 20% afterward.

Casey’s also announced a substantial dividend increase of 14%. As Casey’s share price has performed well, large dividend increases have become common, with this marking the fourth year in a row that Casey’s has boosted its dividend by 13% or more.

However, while Casey’s dividend has grown quickly, its share price has risen even faster, leaving the stock with a low indicated dividend yield near 0.3%. The company’s next dividend is payable on Aug. 14 to shareholders of record as of the Aug. 1 close. Overall, dividend income is low on the list of reasons to own Casey’s. However, the company’s willingness to strongly increase its capital returns is a nice cherry on top of its impressive underlying performance.

Target: Rebounding Retailer With an Over 3% Yield

Another impressive story in the consumer staples sector is Target (NYSE: TGT). After delivering a return of -25% in 2025, Target appointed a new CEO near the beginning of 2026. So far, the move appears to be paying off. After posting five straight quarters of negative sales growth, Target grew revenue by 6.7% YOY in its latest quarter. Not only did the figure return to positive territory, but it was also Target’s highest sales growth rate in approximately four years.

Target also posted a strong improvement in EPS, which rose 31% YOY to $1.71, handily beating estimates of $1.47.

The company now expects sales growth of nearly 4% for the full year, which would be its best annual growth rate since 2022. As Target works to turn around its business, shares have delivered a return of more than 30% in 2026.

Notably, Target has also announced a small dividend increase of just under 2%, moving its quarterly payout to $1.16. The company’s next dividend is payable on Sept. 1 to shareholders of record as of the Aug. 12 close.

Despite Target’s latest increase being modest, the stock’s dividend yield remains relatively high, near 3.5%.

Target also has a very long track record of dividend increases, having raised its payment for 54 years in a row. With this, Target offers investors a solid dividend yield while also providing upside potential should the recovery in its financial performance continue.

Annaly, Casey's, and Target: Different Flavors of Dividends and Growth

While Annaly, Casey's, and Target offer very different dividend profiles, all are showing a strong desire to return increasing amounts of capital to shareholders. When it comes to Annaly, investors should also know the company can significantly reduce its dividend at times. This happened in 2023, when the firm reduced its dividend by approximately 26%.

Copa Holdings May Be the Airline Stock Built to Break Out

By Thomas Hughes. Article Posted: 6/23/2026.

Key Points

- Copa Holdings has a lot going for it, making it a win for investors seeking growth and capital returns.

- A hub-and-spoke setup enables highly efficient airline operations.

- Analysts are forecasting this emerging market stock to reach new highs in 2026.

- Special Report: The company SpaceX cannot operate without

Copa Holdings (NYSE: CPA) is an airline stock with structural advantages, a strong market position, and capital returns that make it a compelling investment. It is positioned as a leading Latin American service provider, offering emerging-market exposure through a critical infrastructure and services business. Its structural advantage comes from a hub-and-spoke network centered on The Hub of the Americas. That hub is the company’s headquarters at Tocumen International Airport, a centralized location that enables highly efficient operations across the system.

This setup has helped Copa deliver the region’s leading service record and the No. 2 record globally, with an average on-time rate of about 90% and completion rates trending in the 99% range. In addition to the hub-and-spoke model, Tocumen’s central location allows for quick connections, further enhanced by terminal placement. Passengers don’t have to worry about customs or transit when moving from one flight to the next. The company also operates a single-type fleet, which helps control costs by limiting maintenance hassles, training needs, and parts inventory.

Copa Holdings Accelerates Growth in Q1 2026

The $15 Gold Fund That Pays Up to $1,152/Month (Ad)

Gold is hitting record highs, but most investors are leaving income on the table. A $15 fund is quietly paying out up to $1,152 a month to regular investors - no mining stocks, no options, no physical metal required.

Chief Income Strategist Tim Plaehn calls it a breakthrough strategy that transforms gold's rally into reliable monthly payouts. The next distribution is just days away.

Discover the gold income fund before the next payout dateCopa Holdings had a strong Q1, with revenue growing 17% to just over $1 billion, underscoring its strength. The top line exceeded MarketBeat’s reported consensus by a wide margin and accelerated from the prior quarter and year, driven by higher capacity and demand. A bullish detail is that passenger traffic increased 15% on a 14% increase in capacity, helping support margin strength, further aided by improved revenue per mile.

Margin performance was also strong. The company widened its operating and net margins despite higher costs, particularly fuel. GAAP earnings grew at an accelerated 20.5% pace, exceeding the consensus estimate by 73 cents, or nearly 1,650 basis points (bps). Looking ahead, the company issued a cautious Q2 forecast, citing fuel-cost headwinds, but remained positive for the year and forecast 17% revenue growth.

Bullish Cash Flow and Capital Return Outlook Drive CPA Price Action

Copa Holdings' highly efficient business enables healthy cash flow and capital returns, including dividends and share buybacks. Dividends are approximately 40% of earnings and look reliable in 2026, yielding approximately 4.5% with shares trading near historically high levels.

Distribution increases are expected, given the revenue and growth outlook, and they will likely continue at a robust, double-digit pace in the coming years. Share buybacks are less aggressive, but they still add value by reducing the share count by an average of 0.3% over the trailing 12 months (TTM).

Institutional activity is mixed, with the balance bullish but relatively flat on a trailing 12-month basis as of mid-year. However, institutions provide solid support, owning about 70% of the shares, and the analysts are more bullish.

MarketBeat shows increasing coverage, firmer sentiment, and rising price targets, with a consensus Buy rating and a forecast for fresh all-time highs. Short interest does not appear to be a concern. It is slightly elevated at around 4% but not alarming, and is more likely linked to hedging activity than outright bearish behavior.

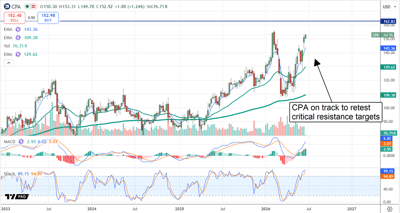

Copa Holdings Advances: Approaches Critical Threshold

Copa Holdings’ price action remains bullish in Q2. The stock is advancing and on track to test resistance at its existing all-time high. Bullish signals in the MACD and stochastic suggest a retest could come soon, potentially by year’s end, and new highs are possible. Setting new highs would be significant, as they would be the first fresh highs in over a decade, opening the door to a much larger move.

In this scenario, the base case is worth the dollar value of the existing trading range, which runs from $120. A move to $280 is possible if a fresh high is set. If not, CPA shares may remain range-bound indefinitely, but that is not expected given the growth and capital return outlook.

Copa Holdings' business is supported by robust demand in a major emerging market region. Latin America is a leading global growth pillar, driven by industrialization and middle-class expansion, which are fueling demand for business and leisure travel. Consistent capital returns are expected over time. The biggest risk for Copa is geopolitical. Not only can conflicts outside the region impair travel demand, but internal issues could also disrupt business. Numerous international agreements enable easy, free-flowing traffic among many of the nations served.

Copa Holdings’ balance sheet is not among its risks. The company maintains low leverage and ample cash, which equated to 40% of TTM revenue at the end of Q1. The likely outcome is that Copa Holdings will continue to execute its strategy, investing in growth while returning capital to investors.

This message is a paid sponsorship sent on behalf of TradeSmith, a third-party advertiser of The Early Bird and MarketBeat.

This ad is sent on behalf of TradeSmith at 1125 N. Charles Street, Baltimore, Maryland 21201. If you’re not interested in this opportunity, please click here.

If you have questions or concerns about your newsletter, please feel free to contact our U.S. based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Place #620, Sioux Falls, SD 57103. United States of America..