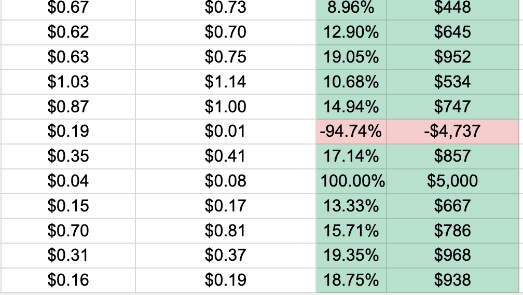

| Dear Traders, What if you could throw out all your charts… moving averages… stochastics… bollinger bands.. candlestick patterns… And actually have a shot at A BETTER WIN RATE? That's what veteran trader Alex Reid did… And over more than 100 vetted real money trades, he hit an 86% win rate… With 11 winners out of the last 12 trades.

*Last live closed trades from October 30th to November 6th, 1 day average hold time. There were also smaller winners, and as you can see, losing trades. We can't promise future gains or against losses. Now, we certainly can't make reckless guarantees when it comes to trading… But Alex has been on fire with this new strategy… And even though he didn't use any of the common tools that most traders use… He wasn't just guessing. Instead he replaced all his old charts and indicators with this proprietary software tool… And you can try it out for FREE right now. It's called the Free Ride Scanner… And if you want to learn the one market signal that it tracks… and how it's achieved such an impressive win rate… And most importantly how you can start using it today… Check out this training right here. To Better Trading, The Wealthpin Team

We develop tools and strategies to the best of our ability but no one can guarantee the future. There is always a risk of loss when trading. Past performance is not indicative of future results. What you will see today are some of the best examples from the public trade research service that utilizes this underlying method. From January 2024 through November 2025 the win rate was 86% with a 40.9% average winner and 23.3% average net return of winners and losers over a 1 day average hold time. There were bigger winners, there were smaller winners and there were losers. Trade at your own risk. Today's editorial pick for you Conagra Stock: Cheap for a Reason, But Capitulation May Be NearPosted On Apr 02, 2026 by Chris Markoch  Conagra Brands (NYSE: CAG) delivered its fiscal Q3 2026 earnings on April 1, and the market’s reaction, a roughly 1.4% decline, may tell investors more than the numbers themselves. The company reported organic net sales growth of 2.4% year over year, a genuine improvement from recent quarters. Yet adjusted EPS of $0.39 fell 23.5% from the prior year, a gap wide enough to give even patient shareholders pause. Table of ContentsHowever, for anyone watching CAG stock closely, today’s session had the feel of capitulation rather than fresh distribution. Volume of 31.2 million shares was nearly twice the average, and the stock is now trading near its lowest levels since 2009. Those sellers who wanted out have largely been flushed. What’s left is a shareholder base that is either convicted in the turnaround thesis or anchored to the dividend, which has a 9% yield as of this writing, and a $1.40 annualized payout that management confirmed it intends to maintain. But before calling this a buying opportunity, investors need to grapple with something deeper than a single quarter’s results. Conagra is a near-perfect specimen of what happens to mid-tier consumer brands caught between a pressured middle class and a company still digesting expensive acquisitions. In today’s K-shaped economy, “nice to have” and “must have” are very different. The K-Shaped Economy Is Conagra’s Real HeadwindConagra’s portfolio, which includes Birds Eye frozen vegetables, Marie Callender’s meals, Hunt’s tomatoes, Slim Jim meat snacks, sits squarely in the middle of the grocery aisle, a place where consumers have never been more price-conscious or more willing to trade down. That is the structural problem this earnings report could not paper over. The K-shaped recovery that defined post-pandemic America has morphed into a K-shaped everyday economy. Higher-income households spend freely on premium items or experiences. Lower-income households are increasingly reliant on private label and deep discounters. Conagra’s brands — aspirationally middle-market, priced above store brands, below true premium — are caught in the squeeze. This showed up clearly in the segment data. Grocery & Snacks organic net sales grew just 1.8%, driven almost entirely by a 4.0% price/mix contribution that masked a 2.2% volume decline. Consumers aren’t rejecting the products outright, but they are buying fewer of them. That volume erosion, sustained across multiple quarters, is the fingerprint of a brand that is losing the value equation in stretched household budgets. Management highlighted its “staples” businesses (i.e., Hunt’s, Vlasic, Hebrew National) as cash generators managed for margin rather than growth. That’s an honest framing. But it also concedes that a meaningful part of the portfolio is in secular decline. M&A Drag and Input Cost Uncertainty Cloud the OutlookAmong the specific headwinds management cited this quarter, two stand out. First, M&A-related expenses, primarily from prior divestitures and restructuring, weighed on corporate overhead. Adjusted corporate expense rose 25.5% year over year, a meaningful drag that depressed the consolidated operating margin even as individual segments showed some resilience. Second, and perhaps more unnerving for forward-looking models, management flagged uncertainty around input costs tied to the U.S. conflict with Iran. Conagra already embedded approximately 7% inflation (including gross tariff impacts) into its FY26 guidance. Any supply disruption affecting energy, packaging, or agricultural commodities could push that figure higher, compressing margins that are already running thin at 10.6% adjusted operating margin, 213 basis points below last year’s level. The company did lower its adjusted equity earnings estimate for Ardent Mills, its flour milling joint venture, from roughly $170 million to roughly $140 million — a $30 million reduction that fed directly into the EPS guidance cut toward the low end of the $1.70–$1.85 range. Where the Bull Case Can Still WinTo be fair to the other side of the ledger, Conagra is not a story without merit. The company’s Frozen and Snacks segments are genuinely showing momentum. Refrigerated & Frozen organic net sales grew 3.6% with volume up 3.9%. However, that’s the only segment in which volume and price moved in the right direction. Frozen single-serve meals held a 52.5% volume share of the category. Frozen vegetables reached 19.2%, both near multi-year highs. The protein snacks business (Slim Jim, Duke’s, Fatty Smoked Meat Sticks) posted 9% dollar growth and 10% volume growth. David Seeds and BIGS delivered 6% dollar and 5% volume gains. These are not commodity businesses; they are on-trend categories with genuine consumer tailwinds around high-protein diets. Free cash flow conversion is also improving — management raised the estimate to roughly 105%, up from 100% at the prior update. Net debt was reduced by more than $800 million versus year-ago levels. If the company can sustain this deleveraging trajectory, it reduces the risk that the dividend gets cut, which is the primary reason remaining shareholders are holding on. Technical Picture: Not a Falling Knife AnymoreFrom a purely technical standpoint, the CAG chart has the look of a stock attempting to form a base after an extended downtrend. The shares touched multi-year lows near the $15 area — a level not seen since 2009 — and today’s intraday low of $15.08 held above prior support. That is a modest but meaningful distinction. The RSI at 35.35 is approaching, but has not yet confirmed, oversold territory. The MACD is marginally positive at 0.0223. That’s not a bullish signal, but at least no longer deeply negative. The signal line at -0.7336 remains well below zero, suggesting the momentum has not yet turned. Volume on today’s session was heavy, which in the context of a multi-month downtrend can be read as exhaustion selling.  This is not a call to buy CAG today. But the stock no longer behaves like a falling knife. Stocks that are in the process of capitulating tend to have high-volume sessions at or near lows, followed by periods of sideways consolidation. If the $15 area holds on subsequent tests, it could represent a longer-term floor, and one worth revisiting as the fundamental picture clarifies. Conclusion: A Dividend Story Waiting for a CatalystConagra is a company in transition, caught between a portfolio that doesn’t perfectly fit the current consumer moment and a balance sheet still being repaired from acquisition-era leverage. Today’s earnings report offered green shoots — organic sales growth returned, Frozen is gaining share, free cash flow is strong — but the macro and cost-structure challenges are real and unlikely to resolve quickly. At current prices near $15.52, the $1.40 annualized dividend yields roughly 9%, a level that markets typically treat as pricing in meaningful risk. Whether that risk is fully priced in is the question every investor in this name has to answer for themselves. The capitulation argument is worth taking seriously. So is the K-shaped economy thesis that has been working against Conagra’s core consumer for the past two years. This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe. StockEarnings, Inc

|

No comments:

Post a Comment