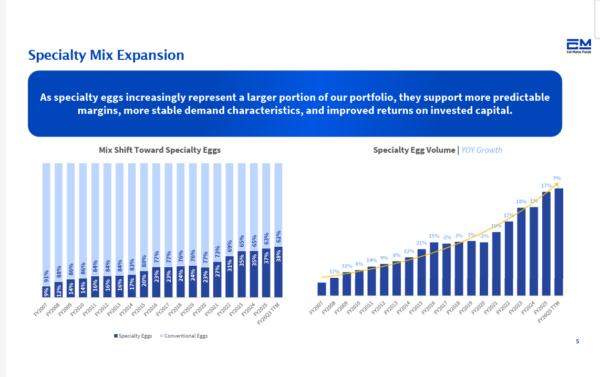

Cal-Maine Foods (NASDAQ: CALM) delivered a strong Q3 FY2026 earnings report on April 1, 2026. But for investors weighing the stock today, “strong” may not be enough to pull the trigger. The numbers were genuinely good. Specialty eggs reached 50.5% of total shell egg sales in the quarter, up 2,610 basis points year-over-year. Prepared foods contributed 9.5% of net sales. Combined, those two higher-margin segments accounted for nearly 53% of net revenue. That’s a milestone that validates management’s long-standing thesis about mix improvement.

Table of Contents

Still, the CALM stock price retreat on the day after the report. shows this is a prove-it story. The analyst consensus for the next fiscal year reflects expectations for significantly lower revenue and earnings than what CALM has posted during the elevated egg-price environment.

That sets up a lower bar to clear, which is a double-edged sword. Easier comparisons could flatter future quarters. But those lower estimates also signal that the market doesn’t yet believe this business has permanently re-rated to a higher earnings level. Until sustained growth in a more normalized price environment is demonstrated, investors have good reason to remain cautious.

I recently sat down for a private meeting with a source connected to global power networks. What he revealed about the current situation in Iran is far different from the headlines you’re seeing on the news. There is a coordinated strategy unfolding—one involving massive shifts in global energy and intelligence circles.

I’ve verified the details and put together a full breakdown of what this means for your portfolio. You need to see the real reason behind this escalation.

Specialty Eggs: The Mix Shift Is Real, and It Matters

The headline story from this earnings report isn’t really the quarterly numbers; it’s the long-term mix shift. In FY2007, specialty eggs were just 9% of Cal-Maine’s volume. By the Q3 FY2026 trailing twelve months, that figure has climbed to 38%. This is a structural change, not a cyclical one.

Why does it matter? Specialty eggs (i..e., cage-free, pasture-raised, organic, and nutritionally enhanced varieties) are sold under fixed-price contracts with retail and foodservice customers. Unlike conventional eggs, which are priced against the volatile Urner Barry commodity index, specialty egg pricing is negotiated and locked in. That means more predictable margins, more stable revenue, and less exposure to the sharp price swings that have historically whipsawed Cal-Maine’s earnings. Management isn’t wrong to call this a quality-of-earnings improvement. The question is whether the market will pay a higher multiple for it, and that remains to be seen.

The Balance Sheet Is a Genuine Bright Spot

One thing that’s hard to argue with is Cal-Maine’s financial position. The company carries essentially no debt and had over a billion dollars in cash and short-term investments at last check. That gives management the flexibility to pursue acquisitions — like the recent $128.5 million Creighton Brothers deal — without stretching the balance sheet.

The capital allocation framework laid out in the earnings report is sensible: reinvest in organic specialty capacity first, pursue M&A second, return excess cash third. That hierarchy is straightforward and consistent. The Creighton Brothers acquisition adds 3.2 million laying hens, including 500,000 cage-free birds, along with liquid egg capacity and a feed mill. It’s a bolt-on that fits the strategy cleanly. For investors who like boring but durable businesses, the balance sheet alone is a reason not to sell.

What the Chart Is Telling You

The daily chart tells an interesting story that the press release doesn’t. CALM stock opened higher on earnings day before selling off sharply, a classic “buy the rumor, sell the news” pattern. But more notable is what happened at today’s close. The stock dropped hard in a long red candle, giving up most of its post-earnings recovery, even as the broader market staged a modest bounce.

That kind of relative weakness is worth noting. It suggests institutional sellers are using strength to exit rather than build positions. The 50-day moving average, currently around $83.54, acted briefly as resistance before the stock fell back below $78. The MACD is crossed bearish and widening slightly. That’s not a crisis signal, but not a green light either. A stock that can’t hold a rally on a beat-and-raise quarter is sending a message. Respect it.

What Could Accelerate the Bull Case

The bull case for Cal-Maine doesn’t require anything exotic. It requires time and execution. If specialty egg volumes continue growing at a high-single-digit rate while fixed-price contracts insulate margins, the earnings-quality story starts to look compelling in a normalized pricing environment.

Eggs also appear relatively insulated from the GLP-1 dietary trend that has weighed on some processed food companies. Protein demand is, if anything, a tailwind. A resumption of volume growth, combined with a couple of quarters demonstrating that margins hold even as conventional egg prices normalize, could shift the narrative from “cyclical windfall” to “durable compounder.” That re-rating is possible. It just isn’t priced in yet.

Conclusion: Hold, Collect the Dividend, and Wait for the Story to Develop

CALM stock earns a Hold here. The business is well-run, the strategy is coherent, and the balance sheet is exceptional. But the stock needs to demonstrate that its specialty-egg thesis translates into durable, mid-cycle earnings power—not just peak-cycle profits dressed up in a better mix.

The variable dividend policy is worth understanding clearly. Shareholders receive one-third of GAAP net income, which produces a yield currently above 3% – ahead of inflation for now. But that payout is directly tied to earnings, meaning a significant income drop could cut the dividend substantially. It’s not a dealbreaker, but it has a different risk profile than a fixed-dividend payer. For patient investors who can live with that variability, Cal-Maine offers a solid business at a reasonable price. Just don’t expect the market to reward it quickly.

StockEarnings, Inc (SE) is a research service not owned or managed by registered brokers and therefore this site does not make any investment recommendations. The information provided in this newsletter is not guaranteed as to the accuracy or completeness. Each user of SE chooses to do trades at their sole discretion and risk. SE is not responsible for gains/losses that may result in the trading of these securities.

This newsletter includes paid advertisements. The source of all third-party content in which SE receives some sort of compensation, is clearly and prominently identified herein as "ad" or "Sponsored". Although we have sent you these advertisements, SE does not specifically endorse any third-party product nor is it responsible for the content of the advertisement or the experience with the third-party advertiser. Furthermore, we make no guarantee or warranty about what is advertised.

All investments involve risk, losses may exceed the principal invested, and the past performance of a security, industry, sector, market, or financial product does not guarantee future results or returns. Please click here for SE Disclaimers.

StockEarnings Inc.33 SE 4th St, Suite 100,Boca Raton, FL 33432 USA ! W;887, 6 STOCKS

.jpg)

No comments:

Post a Comment