Before the Giants Come Knocking

There's something satisfying about spotting a company early.

Before the headlines.

Before the institutions.

Before a larger player decides it wants in.

In biotech, that moment often comes when a start-up builds something protected, differentiated, and positioned inside a massive market.

Large pharmaceutical companies regularly use acquisitions and licensing to grow, especially when innovation can strengthen their pipelines.

One under-$1 biotech fits that early profile.

- 5 patents protecting its drug and delivery platform

- Targeting a well-studied DNA repair pathway in cancer

- Designed to complement existing therapies

- Advancing toward human testing

- Valuation near $46M inside a projected $500B market

No one can predict how the story unfolds.

But it can feel good to spot an underdog before the spotlight hits.

See the Company Before the Giants Do >

Trash to Treasure: 3 Waste Removal Stocks to Minimize Volatility

Authored by Dan Schmidt. Published: 3/22/2026.

Key Points

- Waste removal stocks often perform well in volatile times due to inelastic demand for services and long-term contract agreements.

- While the industry is highly-concentraded, the incumbents have unique advantages due to regulatory compliance hurdles.

- Waste Management, Republic Services, and Clean Harbors are three waste removal companies with upside in the current market environment.

- Special Report: Elon's "Hidden" Company

If you hate taking out the trash, welcome to an exclusive club: everyone. Trash removal is always a consideration when renting or buying a new home because we all produce it and need it picked up in one form or another. Since demand for trash removal is largely inelastic, the companies that provide these services typically generate steady, if unspectacular, revenue. The waste removal industry, however, has a few other advantages that set it apart from typical consumer staples companies:

- Regulatory and environmental burden - Removing trash from a home is usually straightforward, but managing waste for businesses and governments is another matter. The waste disposal industry is highly regulated, with strict standards and high barriers to entry. Opening a new landfill is a multi-year process, so incumbents operate with oligopolistic pricing power.

- Long-term revenue streams - Waste removal companies typically operate under long-term contracts that lock in consistent revenue and tend to hold up during economic slowdowns. Businesses usually book contracts for one to three years, while larger companies and municipalities often sign five- to seven-year agreements. Contracts can be flat or variable rate and frequently include clauses for regulatory fees and fuel surcharges (increasingly important as oil prices change).

This combination of essential demand and regulatory barriers often makes the sector a solid defensive investment. Historically, waste management firms have performed relatively well during market corrections and periods of volatility. With the Iran conflict ongoing and the S&P 500 hovering near its 200-day moving average, market fluctuations are likely to continue, making waste service companies intriguing options for investors.

3 Steady Waste Removal Stocks With Upside

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…The industry's oligopolistic structure means only a handful of waste-removal companies trade publicly on U.S. exchanges, limiting investment choices. With that in mind, here are three companies that offer an attractive mix of upside potential, consistency, and dividend income, while also helping to limit exposure to fluctuating fuel costs.

Waste Management: The Cashflow King

Waste Management Inc. (NYSE: WM) is the largest waste removal company in the U.S., both by market cap (about $94 billion) and by the number of landfills, transfer stations, and recycling facilities it operates.

It is also very shareholder-friendly, a trend likely to continue after reporting strong free cash flow of $2.94 billion in Q4 2025.

Management expects free cash flow to grow by more than 30% in 2026 and is backing that forecast with a 14.5% dividend increase and $3 billion in share buybacks.

The company is further insulated from Strait of Hormuz-related energy disruptions through surcharge mechanisms that pass diesel and compressed natural gas (CNG) price increases on to clients.

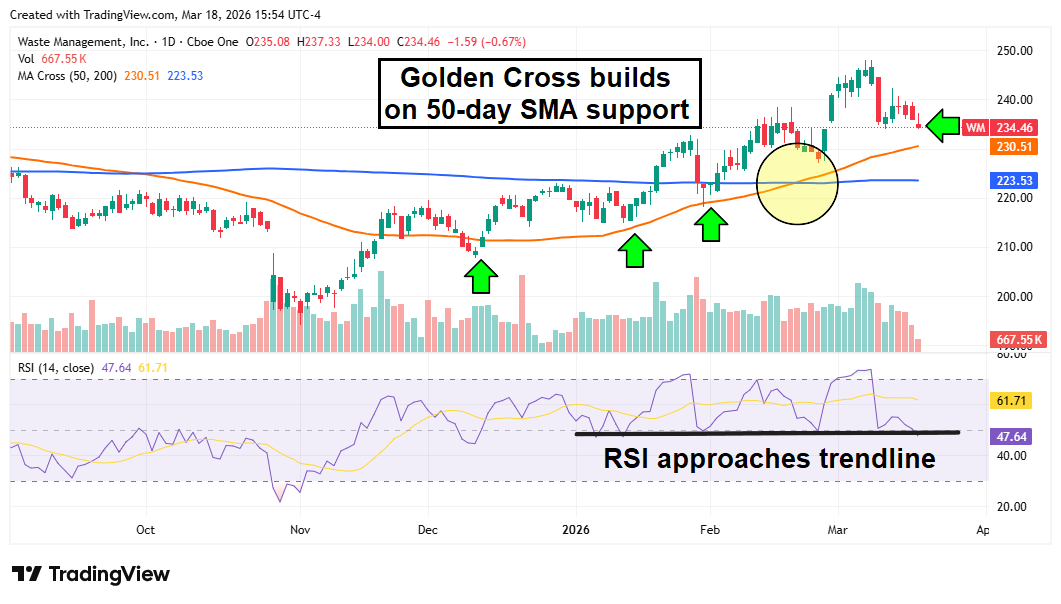

WM shares show the makings of a solid technical uptrend, with a bullish Golden Cross and healthy support at the 50-day moving average.

A move into overbought territory on the Relative Strength Index (RSI) triggered a brief pullback. The share price is once again approaching the 50-day moving average support level, which could be a favorable entry point for new buyers. The dividend now yields 1.62%, with a 56% dividend payout ratio and a 22-year streak of payment increases.

Republic Services: Low Leverage and Dividend Resilience

Republic Services Inc. (NYSE: RSG) often plays second fiddle to WM because of its smaller market cap, lower dividend yield, and fewer locations.

Still, RSG offers some advantages WM does not: an earnings beat in Q4 2025 and a cleaner balance sheet.

RSG carries less debt and has engaged in less M&A activity, which can mean slower growth but also lower financial leverage and risk.

RSG's dividend yield is lower at 1.13%, but its DPR is a healthy 36%, suggesting room for future dividend increases.

RSG uses a fuel-surcharge model similar to that of its larger competitor, helping to mitigate the impact of rising oil prices.

RSG shares have lagged WM so far in 2026, and the technicals show some tension between buyers and sellers on the daily chart. If volatility remains elevated, RSG could continue the breakout that began last November.

The stock appears to have found support at the 50-day moving average, and the RSI has returned to levels that previously marked short-term lows. A sustained move above the 200-day moving average could be the next catalyst.

Clean Harbors: Upside From Government Contracts

Clean Harbors Inc. (NYSE: CLH) isn't a traditional collection-and-disposal company like RSG or WM, but it offers more upside potential.

More than 75% of the company's revenue comes from Environmental Services, a more cyclical segment than Collection and Disposal. Still, Clean Harbors benefits from reliable, multi-year government contracts.

The company has a multi-year agreement with the Department of Defense for polyfluoroalkyl substances (PFAS) filtration services, with an option to expand each year.

PFAS are dangerous "forever chemicals" that may contaminate water at more than 700 military bases. Clean Harbors is the only company capable of providing all three phases of PFAS filtration, remediation, and incineration, giving it a deep moat for these services and an edge when pursuing additional government work.

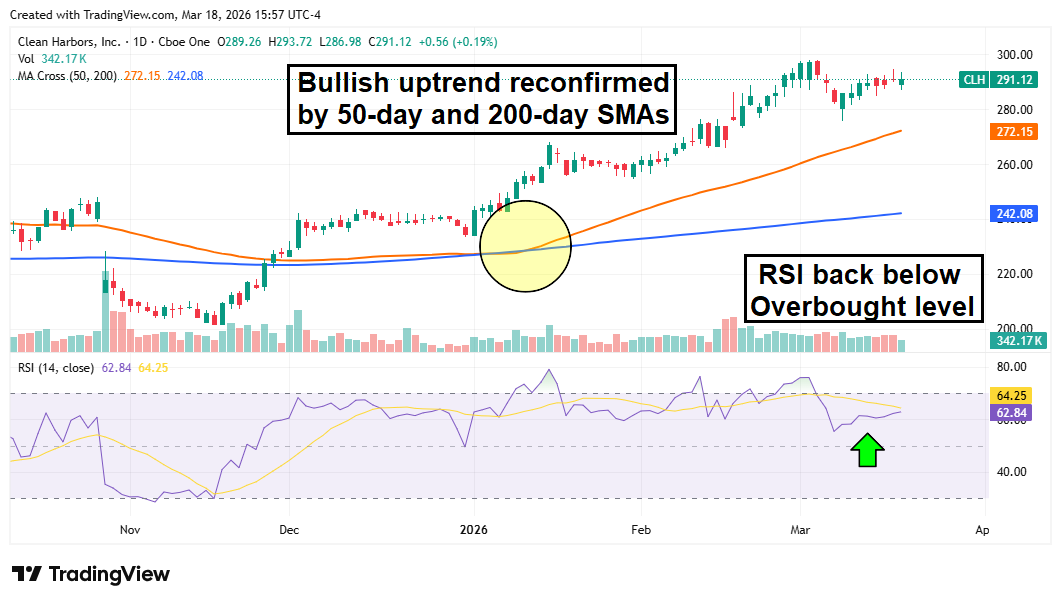

Investors tend to favor companies with steady government contracts, and CLH shares have gained more than 20% year to date. The stock is in a strong uptrend, trading well above both the 50-day and 200-day moving averages, and the RSI has cooled from overbought levels.

With the DoD now involved in a prolonged conflict with Iran, defense budgets may rise further beyond the administration's initial requests earlier in the year, which could translate into additional revenue for Clean Harbors' coffers.

The AI Gatekeeper: TSMC's Chokehold Signals Dominance

Written by Jeffrey Neal Johnson. First Published: 3/25/2026.

Key Points

- TSMC's technological leadership in advanced chip manufacturing creates a significant and durable competitive advantage over its industry rivals.

- Overwhelming demand from the AI sector for its cutting-edge production and packaging technologies is fueling exceptional financial performance.

- TSMC’S foundational position as the primary manufacturer for top technology firms makes it a central pillar of the global artificial intelligence supply chain.

- Special Report: Elon's "Hidden" Company

A significant development is sending ripples through the artificial intelligence (AI) sector. NVIDIA (NASDAQ: NVDA), a titan of the industry with a multi-trillion-dollar valuation, is reportedly being forced to redesign its next-generation Feynman AI platform.

The reason isn't a design flaw or a sudden market shift, but a fundamental manufacturing reality: Taiwan Semiconductor Manufacturing Company (NYSE: TSM), the sole producer of its most advanced chips, is operating at full capacity.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…This dynamic—where the industry's most powerful designer must conform to its manufacturer's production schedule—reveals the real power structure in the AI hardware ecosystem.

It points directly to TSMC's commanding position and makes a clear, data-driven case for its role as a cornerstone investment in the technology revolution.

The Unbreakable Bottleneck

A production crunch is creating a multi-year waiting list for the world's most advanced semiconductors. The bottleneck centers on TSMC's 2-nanometer (2nm) and upcoming A16 process nodes—the technologies expected to power the next leap in AI. Demand from high-performance computing (HPC) and AI customers is so intense that it has forced even top-tier clients like NVIDIA into a queue, producing a backlog that could last years. This is not a minor delay; it is a structural constraint that underscores TSMC's unmatched influence over the industry's trajectory.

This dominance stems from a deep, costly technological moat that competitors struggle to cross. It is the product of long-term strategy and relentless investment, not a temporary lapse in capacity.

- Leading-Edge Manufacturing: Producing chips at the 2nm scale—where billions of transistors fit on a fingernail—is a monumental engineering feat. A single fabrication plant (fab) capable of this work can cost upward of $20 billion and requires more than a decade of focused research and development to perfect. That level of capital intensity creates an enormous barrier to entry, and TSMC's sustained investment has left it years ahead of rivals. Even as Moore's Law has slowed, TSMC continues to push the boundaries of physics, making its fabs the go-to option for companies seeking maximum performance.

- Advanced Packaging Power: TSMC's edge extends beyond wafer production to advanced packaging technologies such as Chip-on-Wafer-on-Substrate (CoWoS). As individual chips become harder to shrink, performance gains increasingly come from connecting multiple smaller chips, or chiplets, into a single processor. CoWoS is the gold standard for this approach, and AI-driven demand for advanced packaging far outstrips supply. By controlling both cutting-edge chip production and the packaging needed to assemble them, TSMC creates a dual bottleneck that effectively locks in its most important customers.

Competitors like Intel (NASDAQ: INTC) and Samsung (OTCMKTS: SSNLF) are investing heavily to close the gap, but they remain years behind in matching TSMC's performance, manufacturing yield, and scale at the leading edge. That gap gives TSMC a clear and durable competitive advantage for the foreseeable future.

From Microchips to Megaprofits

TSMC's technological supremacy translates directly into strong financial performance, creating a fortress-like balance sheet that rewards investors. With a market capitalization of roughly $1.75 trillion, its scale is immense, but the operational metrics tell the fuller story.

TSMC controls more than 70% of the global market for advanced semiconductor manufacturing—a near-monopolistic share that grants significant pricing power. That power shows up in an industry-leading net profit margin that exceeds 45%. For context, many successful technology companies operate with net margins in the 20–30% range.

Keeping over 45 cents of every revenue dollar is exceptional and indicates the premium customers are willing to pay for TSMC's services. This financial strength is reinforced by an impressive return on equity of nearly 35%, a measure of how effectively management deploys shareholder capital to generate profits.

Recent earnings reports show that the High-Performance Computing (HPC) segment—which includes AI chips designed by NVIDIA and others—is TSMC's primary growth engine, confirming that the company is a primary beneficiary of the AI boom.

Strategically, TSMC is using its financial strength to solidify global leadership and manage geopolitical risk through targeted expansion. The announced investments in new fabs—roughly $40 billion in Arizona and additional multi-billion-dollar capacity in Japan—are more than defensive moves. They are strategic plays to deepen partnerships with key customers, secure government incentives, and protect future revenue streams, further reinforcing TSMC's indispensable role in the global supply chain.

Investing in the Irreplaceable

The manufacturing constraints forcing a redesign at one of the world's top technology companies are not a sign of weakness at TSMC, but the ultimate proof of its strength. TSMC's deep technological moat, dominant market share, and fortress-like financials make it a unique, foundational asset in the global economy. As the central gatekeeper through which nearly all of the world's most advanced technology must pass, TSMC is a compelling consideration for investors looking to build a position in the foundational layer of the AI revolution.

This email message is a sponsored email for i2i Marketing Group, LLC, a third-party advertiser of MarketBeat. Why did I get this email?.

We are not securities dealers or brokers, investment advisers or financial advisers, and you should not rely on the information herein as investment advice. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent corporate information. Further, readers are advised to read and carefully consider the Risk Factors identified and discussed in the profiled company's SEC and/or other government filings. Investing in securities, particularly microcap securities, is speculative and carries a high degree of risk.

If you need help with your account, feel free to email MarketBeat's U.S. based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl., Suite 620, Sioux Falls, S.D. 57103-7078. United States..

No comments:

Post a Comment