Dear Fellow Investor,

The Iran War didn't just make headlines.

It broke the gold market wide open.

Gold is already above $5,000 and surging.

But the metal isn't where the real money gets made.

There's one tiny company sitting on more gold than France, Italy, and China combined.

It moves 10x faster than the metal.

And right now, it's still trading at a 99% discount to what it's actually worth.

A briefing with the ticker is waiting for you.

Go here for the full gold briefing — including the stock name and buy-up-to price >>>

"The Buck Stops Here,"

Dylan Jovine, CEO & Founder

Behind the Markets

IonQ in Rebound Mode: Buy the Thesis, Respect the Risk

Author: Thomas Hughes. Article Published: 3/3/2026.

Key Points

- IonQ's fiscal Q4 results beat expectations, but the stock's path forward depends on more than just one strong quarter.

- A major acquisition and surging government-adjacent demand could reshape the company's trajectory—if execution follows through.

- Institutional buying and elevated short interest are setting up a potential technical catalyst, though analysts aren't fully on board yet.

- Special Report: [Sponsorship-Ad-6-Format3]

IonQ's (NYSE: IONQ) Q4 2025 earnings report may or may not signal a shift in the quantum narrative. What it does show is demand for its services and execution of its strategy, positioning the company to potentially dominate the industry. The strategy has refocused on the chips that drive quantum, a full-stack approach and a unified platform for users. The critical details include strong revenue and guidance, and a potential stock-price rebound that could add as much as 80% to 100% to the share price.

There are clear risks. The underlying technology already generates revenue but remains in early stages. The company is not yet profitable, burns cash, and may need to dilute shareholders in coming years. A 2025 share offering left IonQ well-capitalized for now, but the company's shares outstanding rose roughly 70% year over year, so any equity gains could be short-lived. Although IonQ holds mostly cash and plans technology investments, expansion and acquisitions, ongoing operational losses could deplete that cash quickly.

Economist who Predicted 2008 and 2020 Crashes: "Prepare for AI Meltdown" (Ad)

He's the famous economist and best-selling author who predicted the 2008 meltdown just three weeks before Lehman Brothers imploded and the Covid meltdown just three weeks before the stock market suffered the fastest drop in history. He's now predicting we're about to see an AI meltdown of historic proportions, similar to what happened in 2000 during the dotcom bust when the stock market crashed almost 80%, ruining the retirement of millions of Americans, warning that the most important AI company in the world is about to go bust in a meltdown 10 times bigger than Lehman Brothers.

See the five simple steps to prepare nowThe acquisition pipeline includes SkyWater Technologies. Valued at $1.8 billion in cash and stock, SkyWater will add domestic foundry and development capabilities, giving IonQ greater control of its supply chain. SkyWater also brings existing clients and revenue and the potential to be profitable, which could accelerate IonQ's timeline.

Analysts Respond Favorably: Limit IonQ Upside in 2025

The analysts' response to the Q4 results is broadly bullish, with many citing quadruple-digit revenue outperformance, a growing backlog and a strong guide — but they largely did not raise price targets. The six revisions MarketBeat tracked in the first week after the release included four price-target reductions and one newly set target; most fell at the low end of analysts' ranges. That activity constrains upside, potentially capping gains at consensus or below. Still, the stock retains rebound potential — in the 20% to 50% range — and that could materialize quickly given other factors.

Institutional and short-selling data point to the possibility of a short-covering rally or squeeze. The short interest is off its peak but rose sequentially in the latest report, remaining near long-term highs around 25%. That is a substantial headwind and could cap gains, but heavy institutional buying helps offset the risk. Institutional investors now own more than 40% of the stock and have been buying aggressively over recent quarters.

MarketBeat data show the institutions are buying at a pace of more than $3 for every $1 sold, with buying and total activity ramping to record levels in early Q1 2026. That provides a solid support base: buying is broad-based across institutional groupings, not concentrated only in index funds, and could act as a tailwind for price action during a rebound. Institutional activity aligns with a technical price floor and the early-2026 rebound; technically, the market appears well-supported, with rising volume as prices advanced.

Long Path to Profits Raises Risks for Investors

The Q4 results were solid, and analysts are raising their estimates. Improvements appear in both near- and long-term forecasts, but the key hurdle is profitability. IonQ is expected to improve leverage over time, yet profits are not projected until well into the next decade. That opens the company up to volatility, execution risk, and disruption. IonQ will need to execute near-perfectly; any delays or setbacks would likely show up quickly in the share price, as seen in the price action.

Disruption could come from a pure-play competitor, but is perhaps more likely from existing tech blue chips with ample cash to deploy. For example, NVIDIA (NASDAQ: NVDA), which collaborates with IonQ on integration, has the balance sheet to acquire IonQ multiple times over and still pursue its core strategies, including heavy investment in integrating quantum with traditional systems.

Other Magnificent Seven companies, including Alphabet (NASDAQ: GOOGL) and Microsoft (NASDAQ: MSFT), are also investing heavily in quantum. Alphabet is often viewed as the biggest threat, focused on fault-tolerant systems and its Willow chip. Released at the end of 2024, the Willow chip represented a meaningful advancement, showing improved error reduction as systems scale.

Freeport-McMoRan's Rally Is Over—But the Bull Case Isn't

Author: Chris Markoch. Article Published: 3/6/2026.

Key Points

- Freeport-McMoRan’s Grasberg restructuring secures operations through 2041 but reduces its economic ownership, creating both stability and lower earnings leverage.

- Rising copper demand from EVs, data centers, and electrification supports the long-term bull case for FCX stock.

- After an 80% rally in four months, technical indicators suggest FCX stock may pull back toward the $55–$57 range before its next move higher.

- Special Report: [Sponsorship-Ad-6-Format3]

Freeport-McMoRan Inc. (NYSE: FCX) entered 2026 riding a wave of bullish sentiment. The company is one of the world's leading copper miners at a time when basic materials — and mining stocks in particular — are seen as relatively safe investments.

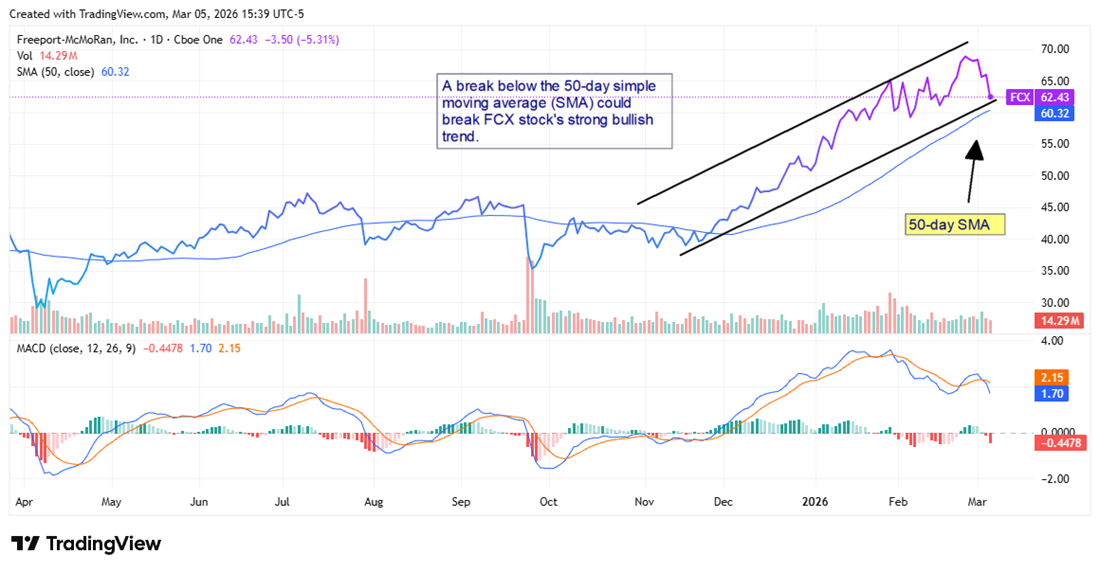

However, after surging nearly 20% following its Jan. 22 earnings report, FCX has given back almost all those gains. The stock recently closed near $62, hovering near its 50-day moving average of roughly $60.

Economist who Predicted 2008 and 2020 Crashes: "Prepare for AI Meltdown" (Ad)

He's the famous economist and best-selling author who predicted the 2008 meltdown just three weeks before Lehman Brothers imploded and the Covid meltdown just three weeks before the stock market suffered the fastest drop in history. He's now predicting we're about to see an AI meltdown of historic proportions, similar to what happened in 2000 during the dotcom bust when the stock market crashed almost 80%, ruining the retirement of millions of Americans, warning that the most important AI company in the world is about to go bust in a meltdown 10 times bigger than Lehman Brothers.

See the five simple steps to prepare nowFor investors who missed the November 2025 rally, this sell-off may seem puzzling.

Dig deeper and a more nuanced picture emerges: the long-term bull case largely remains intact, supporting a buy-the-dip thesis for FCX. Still, near-term valuation concerns and geopolitical risks could push the stock lower before it recovers.

The Grasberg Factor: A Calculated Bet on Indonesia

The Grasberg mine in Papua, Indonesia, ranks among the world's largest copper and gold mines and sits at the center of Freeport's bull case.

On Feb. 18, Freeport announced that it had restructured its relationship with the Indonesian government. Specifically, the company traded its majority stake in Grasberg to state-owned PT Indonesia Asahan Aluminium (Inalum) in exchange for operational continuity and a long-term contract of work.

The deal locked in Freeport's right to operate through at least 2041, providing a long runway as copper demand rises (see where copper demand is headed).

It was pragmatic dealmaking under pressure, and shareholders pushed FCX to an all-time high within a week of the announcement.

But as the stock has pulled back, investors appear to be weighing the trade-off: Freeport now holds a minority economic interest in Grasberg rather than a majority, which reduces per-share earnings leverage to the mine's output.

Grasberg's ore body is so large and its gold and copper grades so rich that even a minority interest generates meaningful cash flow. This is not a diminishing asset, and that cash flow should become more valuable as the world electrifies and demand for copper rises.

The Copper Demand Thesis Is Not Going Away

The long-term bull case for FCX rests on copper, and that story remains strong. In 2022 the focus was electric vehicles (EVs) and renewable-energy infrastructure; by 2026 it also includes grid-scale battery storage and expanding data centers (read more).

Copper demand is surging while supply is not keeping pace. There are three key reasons:

- New large copper deposits are increasingly rare.

- Many are located in geopolitically difficult regions.

- The accessible ones require years and billions of dollars to bring online.

Freeport, with world-class assets in Arizona, Peru, and Indonesia, is one of a small number of companies capable of meeting that demand at scale.

Analysts broadly agree that the structural supply deficit expected in the late 2020s remains likely. Short-term macro noise — concerns about Chinese growth and the effects of higher interest rates on industrial demand — can influence prices, but the electrification tailwind is generational.

Gold Adds a Second Engine

Freeport's exposure to gold strengthens the bull case. Grasberg isn't a copper operation that also yields some gold — it's a true dual-commodity powerhouse.

Today that matters: gold is in a multi-year bull cycle driven by central-bank buying, de-dollarization trends, geopolitical uncertainty, and investor demand for hard assets. Sustained higher gold prices make Grasberg's gold output an increasingly material contributor to Freeport's earnings.

Gold exposure partially hedges copper volatility and provides FCX with revenue that is less tied to industrial demand. For long-term investors, that dual-commodity profile differentiates Freeport from many peers.

The Chart Is Sending a Warning Signal

The technical picture offers a cautionary note for short-term positioning. FCX rallied strongly from roughly $38 in October 2025 to a peak just above $70 in early February 2026. A move of more than 80% in roughly four months almost always requires consolidation.

The moving average convergence/divergence (MACD) has crossed bearish, with the signal line pulling away from a declining MACD line. Combined with the stock breaking below its recent trading range, momentum favors more downside—or at best a sideways grind—before the next leg higher.

The 50-day moving average at $60.32 represents the first meaningful support level. A sustained break below that would open the door to a test of the $55 area, which was a prior consolidation zone on the way up.

to bring you the latest market-moving news.

This message is a paid sponsorship from Behind the Markets, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

Copyright 2006-2026 MarketBeat Media, LLC dba TickerReport. All rights reserved.

345 North Reid Place #620, Sioux Falls, S.D. 57103-7078. United States of America..

No comments:

Post a Comment