Editor's Note: Louis Navellier, the quant legend who recommended Nvidia in 2005, just ran a live AI demo that left his research team stunned. Click here to watch it now or read more below.

Dear Reader,

I put the paid version of ChatGPT head-to-head against the FREE version of Elon's Grok.

It wasn't even close.

Grok produced dozens of picture-perfect results while ChatGPT struggled to conjure even one.

But what really floored me wasn't the demo itself. It's what's behind the technology.

In just 19 days, Elon built a system that Oracle executives said was impossible. He connected 200,000 GPUs in a 114-acre facility on the Tennessee-Mississippi state line — and created what Nvidia's CEO calls "superhuman" AI.

Competitors are literally flying spy planes overhead to figure out how he did it.

And one tiny company's technology was central to the entire feat. And it's 49 times smaller than Tesla.

The last time a tech shift this big created new supply chain winners, early investors had the chance to see extraordinary gains. Lithium Americas: 1,452%. NIO: 1,755%.

P.S. The last time my system helped me identify a company this deeply embedded in a major tech buildout, early investors had a shot at 3X returns within 18 months.

Home Depot: Post-Earnings Rally Fades, What's Next For HD Stock?

Posted On Feb 25, 2026 by Chris Markoch

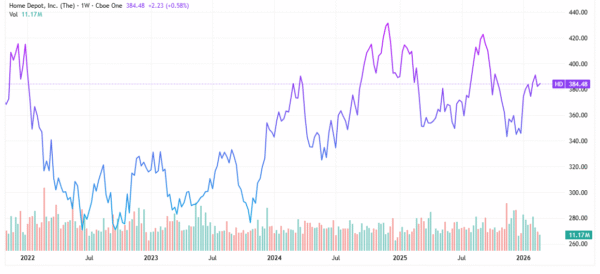

Home Depot (NYSE: HD) stock bounced over 4% in early trading after the home improvement company posted a beat on the top and bottom lines in its Q4 2026 earnings report. On the top line, Home Depot reported $38.20 billion, edging out estimates for $38.10 billion. The bottom line was even stronger with adjusted earnings per share (EPS) of $2.72, beating analysts' forecasts by 20 cents.

Table of Contents

However, as many investors have learned about price action around earnings reports, it's not how you start, but how you finish. By the time the trading session ended, HD stock had given up about half of that gain as investors had time to dig into the report.

To be clear, the bottom line beat was significant. It was the first quarter in Home Depot's 2026 fiscal year that it beat analysts' earnings expectations. But the report wasn't without blemishes. For example:

The $38.20 billion was approximately 4% lower than the $39.70 billion on a year-over-year (YoY) basis.

Total customer transactions were down 8.5% year over year.

Net income declined by over 14% YoY.

As I've noted before, initial trading at the market open is largely controlled by high-speed algorithm programs. When it comes to earnings reports, these "traders" look for distinct numbers. If the numbers are better than expected, buy orders are issued. The opposite is true of selling.

But that buying and selling happens without much human analysis. That happens throughout the day, and after investors have had a chance to hear what the company's management said on the earnings call. That's where this sell-off may have started.

However, as noted above, Home Depot's report had some blemishes. In this case, management used its conference call to provide context. The reasons given probably sounded familiar to investors: higher rates, lower housing turnover, and a consumer who's feeling uncertain about the economy (and perhaps their job). That means customers are putting off larger projects, which means YoY revenue comparisons are likely to be negative.

DA Davidson was quick to raise its price target for HD Stock to $445 from $407. That price target is about 10% above the consensus price target of $410.87. That means they likely buy into Home Depot management's outlook for the current quarter. Spring is usually the company's best quarter. And with consumers supposedly getting record-high tax returns, that may inspire home improvement projects.

The Macroeconomic Data Remains Cloudy

There are times when my background in sales and marketing leads me to a contrarian opinion. The fading of HD stock after its initial earnings pop may not make my opinion contrarian, but you don't have to dig that hard to believe that 2026 (Home Depot's 2027 fiscal year) may look a lot like last year, at least in the first half.

Consumers on the descending leg of the K-shaped economy are under pressure. And as Home Depot's results are showing, even consumers on the ascending leg of the K may be feeling more "choiceful" – to use the buzzword of this quarter. That means it's more likely that consumers will choose to use their tax refunds for practical alternatives such as paying down debt. Or at best, saving the money until they feel better about things.

That's called understanding buyer behavior. When it comes to the economy, it's not about what the numbers say but how consumers "feel" about the economy. Right now, perception – whether accurate or not – is reality.

Now, none of this is to say Home Depot is a failing company. Nor am I saying that management doesn't owe it to its Board of Directors and its shareholders to provide reasons to believe areas of concern won't linger.. Hope sells, or at least keeps investors interested.

Why the Second Half May be Better

Here's why things could be looking up for Home Depot in the second half of the year. The latest read on inflation showed that the rate of inflation at 2.4%. That continues to trend lower, albeit slowly.

However, the Truflation US CPI Inflation Index comes it at 0.95%. The Truflation Index has proven itself to be a reliable leading indicator for future readings of the Consumer Price Index (CPI). And it's showing that there is ample evidence that real inflation is below the Federal Reserve's preferred target right now.

That fact, along with the likely (but not guaranteed) confirmation of Kevin Warsh as the next Chair of the Federal Reserve, means interest rates are likely to move lower, and perhaps by more than some analysts expect. Consumers won't feel that right away, but by late summer, sentiment – and buyer behavior – may improve

Also, analysts are generally bullish on HD stock and institutions have been accumulating, albeit not very aggressively. Nevertheless, inflows outpace outflows by over 2:1.

That's likely to keep a solid floor on HD stock. That's likely to be enough to keep investors interested, particularly income-oriented investors who will collect the company's dividend, which currently has a payout of $9.20 per share on an annual basis.

A Stock Waiting on Sentiment, Not Fundamentals

Home Depot's latest earnings report shows a company that is still fundamentally strong but operating in a demand environment driven more by psychology than necessity. Big-ticket home improvement projects tend to follow confidence in housing values, job security, and borrowing costs—all areas that remain uneven.

If inflation continues to cool and interest rates ease into the second half of the year, Home Depot could see a rebound in discretionary spending that reignites growth comparisons. Until then, HD stock may trade sideways as investors collect its reliable dividend and wait for clearer macro signals. In that sense, Home Depot isn't broken—it's cyclical, and currently in the waiting phase of the cycle.

This is a PAID ADVERTISEMENT provided to the subscribers of Daily Stock Signals Free Newsletter. Although we have sent you this email, Daily Stock Signals and StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us. If you no longer wish to receive email from DailyStockSignals.com, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

No comments:

Post a Comment