Here's a simple question: Americans consider financial advisors the #1 most trusted source for financial guidance. Yet engagement has been plummeting since 2020, with only 39% of the population relying on advisors or investment managers. | The problem isn't a lack of trust—but a lack of connection. | Based on findings from the Allianz Center for the Future of Retirement's 2025 Annual Retirement Study, financial professionals dominate trust rankings at 59%, outperforming financial institutions (54%), education classes (39%), and friends and family (35%). They outperform AI tools and Reddit by 45 points each. | Investors know who can help them. They're just hesitant to ask. |

|

| | But Engagement Is Cratering | The drop in engagement is alarming: from 49% in 2020 to 38% in 2025—an 11-point decline, or a 22% decrease, during a period when retirement planning became objectively harder. Over the past five years, markets have whipsawed, inflation has surged, and healthcare costs have exploded. Meanwhile, tax rules have continued to change. | So why aren't investors connecting with advisors? |

|

| | | | | Buy This AI Stock Tomorrow Morning? | | A former hedge fund manager known for spotting early winners is sounding the alarm once again. He called Netflix at $7.78 (up 4,200% since), Apple at $0.35 (up 20,000%), and Amazon at a split-adjust $2.41 (up 3,200%). | Now he's turning his focus to a little-known AI company that just earned a near-perfect score in his new proprietary stock grading system. In a brand-new presentation, he reveals the name, ticker symbol, and why this could be the smartest AI move of the year... especially if you're over 50. | Click here to watch it before word gets out. |

| |

| | |

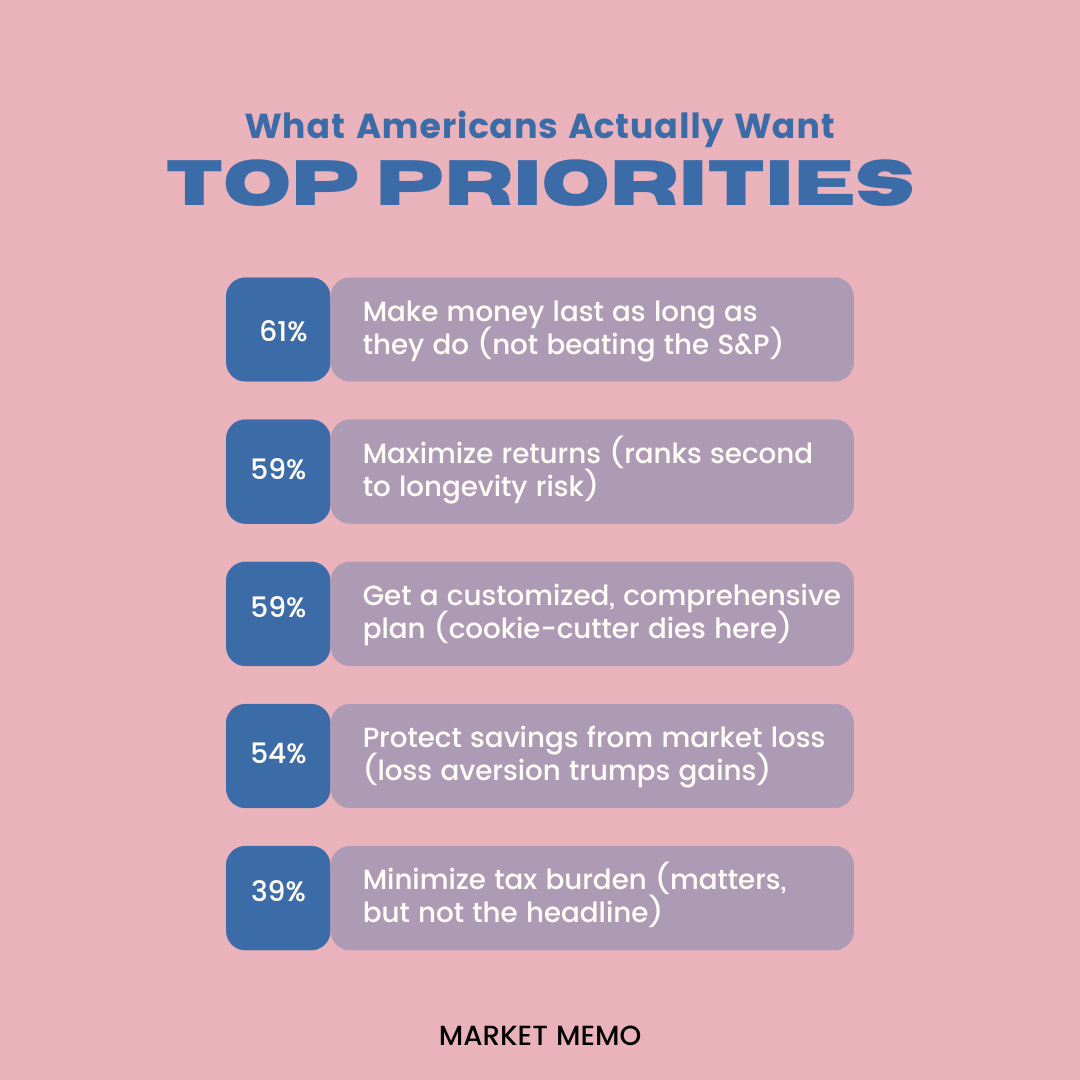

| What Americans Actually Want |  | Top priorities of American investors |

| The Real Gap: Being Known vs. Being Managed | Here's where it gets interesting. Americans aren't just hiring portfolio managers—they're looking for someone who gets them: | 43% want recommendations that reflect their real lives, not idealized textbook scenarios. Real life is messy. Real budgets have gaps. Real spending includes the occasional splurge that doesn't fit neatly into a Monte Carlo simulation. 39% value empathy and understanding of their financial struggles. They want advisors who acknowledge that saving 15% of income may be mathematically sound but practically impossible when supporting both aging parents and children. 37% want to feel known as a person, not just a risk tolerance score. Their financial decisions connect to family obligations, legacy goals, and personal values that don't show up in quarterly statements. 37% want their values and beliefs considered in planning. ESG isn't just an acronym—it's about aligning investments with what matters beyond returns. 37% want advisors with specialized expertise, such as retirement planning or budgeting, rather than generalists trying to be everything to everyone.

|

|

| | The Cookie-Cutter Problem | Americans perceive financial advice as one-size-fits-all. That approach works for accumulation—save 15%, max out your 401(k), buy index funds. But retirement distribution can't be standardized. Health, Social Security timing, legacy goals, and family obligations vary widely. | Generic advice for complex problems feels inadequate—so people avoid advice altogether. |

|

| | The Planning Gap Amplifies the Problem | This trust paradox exists alongside troubling planning gaps: | 47% don't have a written financial plan. 59% don't know what else they should be doing beyond contributing to a 401(k). 45% have no idea how to turn savings into retirement income. 53% believe simply having a retirement account will be enough (it won't).

| These aren't gaps Google can solve. They're strategic planning gaps that require customized guidance. Yet the people who need professional help most are often the least likely to seek it. |

|

| | The Opportunity | The gap between perceived value and actual engagement is a positioning problem—not a market problem. | Closing it requires: | Meeting clients where they are—acknowledging messy finances and competing goals. Demonstrating personalization—tying recommendations to real circumstances. Leading with empathy—recognizing that financial stress is emotional. Specializing visibly—being known for retirement income planning. Making outcomes tangible—showing how strategies translate into income, protection, and legacy.

|

|

| | Become An AI Expert In Just 5 Minutes | | If you're a decision maker at your company, you need to be on the bleeding edge of, well, everything. But before you go signing up for seminars, conferences, lunch 'n learns, and all that jazz, just know there's a far better (and simpler) way: Subscribing to The Deep View. | This daily newsletter condenses everything you need to know about the latest and greatest AI developments into a 5-minute read. Squeeze it into your morning coffee break and before you know it, you'll be an expert too. | Subscribe right here. It's totally free, wildly informative, and trusted by 600,000+ readers at Google, Meta, Microsoft, and beyond. | | | The Bottom Line | Americans trust financial professionals more than any other source, yet engagement is at a five-year low. This isn't a crisis—it's an opportunity. | The issue isn't capability or access. It's the missing conversation. Retirement planning feels overwhelming, and investors hesitate to turn to the very professionals they trust most to help navigate it. | For advisors, the door is open—but the approach must change. Lead with understanding, not products. Show personalization, not standardization. Demonstrate how you'll help money last, not just grow. | For Americans nearing retirement: you already know who can help. The question isn't whether to seek guidance—it's whether you're ready to take the step you already know you should. | The trust is there. The need is there. What's missing is the conversation. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|

No comments:

Post a Comment