The geopolitical environment of 2026 demands a departure from the "static" portfolio models of the past, and financial engineering is here to serve that same purpose. | Last week, I explained how STRC preferred shares provide a unique instrument that not only offers a strong dividend but also some stability to your portfolio. This week, we will explore Autocallable Income ETFs. |

|

| | | | | Stop Chasing NVIDIA | | If you're chasing Nvidia, Amazon, or Palantir right now, I've got one word for you: Stop. | Because according to legendary investor Whitney Tilson, AI mania is about to leave millions of investors holding the bag. Whitney just went public with one of his most controversial predictions in years: "The AI boom is real... but the next wave of gains won't come from where everyone expects." | Instead, he believes a stealthy, little-known stock is about to blow past Nvidia in a way few. |

| |

| | |

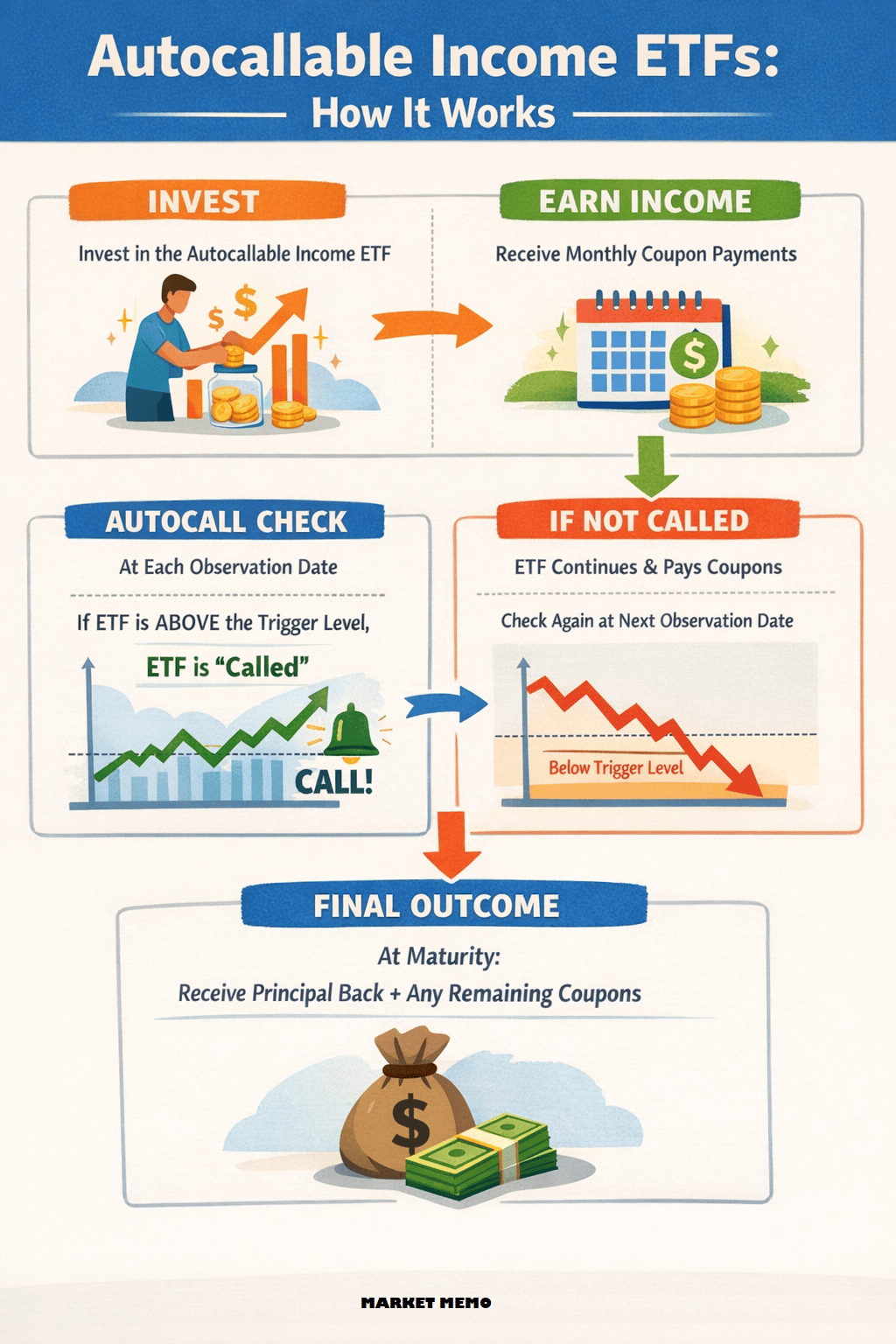

| What is an Autocallable Income ETF? | In simple terms, an Autocallable ETF pays you a high monthly interest rate on your investments (around 1–1.5% per month) as long as the stock market doesn't crash. | The good news: you can earn around 14–18% per year if the market remains stable. The limitation: if the market rises 50%, your gains are capped at those monthly payments. If the market drops more than 30% (the maturity barrier), you could lose money.

| Once a month, the fund checks the market: | | When the term ends (1–3 years): | | This investment vehicle is suitable for investors who need income now and can live without home-run returns. It's not ideal for people building a retirement nest egg or for anyone who may need access to their money during a market crash. |

|

| | How It Works | With J.P. Morgan Global Research forecasting a 35% chance of a U.S. and global recession in 2026, both institutional and retail investors are re-evaluating traditional fixed-income and equity allocations. Autocallable Income ETFs offer a "defined outcome" investing model, which uses derivatives to provide regular income through exposure to a portfolio of autocallable instruments such as over-the-counter (OTC) swap agreements or laddered synthetic notes. | | Historically, individual autocallable notes lacked liquidity and required high minimum investments ($10,000–$100,000). ETFs solved these issues by adopting a laddered approach, holding multiple notes at different entry points to mitigate single-note risk. |

|

| | ETF Framework Components | Reference Index: Payments are based on benchmark index performance, checked monthly. Coupon Barrier: If the index stays above this level, investors receive monthly payments (1–1.5% per month, ~12–18% per year). Autocall Level: If the reference index hits the target on a call observation date, the note matures early, returning the principal plus the final coupon. Maturity Barrier: Principal protection, typically set at -30% or -40%.

| Example: | You invest $10,000. The barrier is -30%. | Month 1: S&P 500 down 15% → Payment of $120. Month 2: S&P 500 down 35% → No payment. Month 3: S&P 500 recovers to down 20% → Payment resumes. End of Year 3: S&P 500 down 25% → Principal returned.

| The coupon barrier affects monthly income, while the maturity barrier determines whether principal is returned at term-end. |

|

| | Key Offerings | Ticker | Issuer | Strategy Focus | Expense Ratio | Key Mechanism | CAIE | Calamos | US Large-Cap | 0.74% | MerQube US Vol Advantage Index (35% VT) | CAIQ | Calamos | Nasdaq-100 | 0.74% | MerQube Nasdaq Vol Advantage Index (35% VT) | ACEI | Innovator | Equity Basket | 0.79% | Laddered OTC Swap Portfolio (30% Barrier) | ACII | Innovator | Index Basket | 0.79% | Worst-Of: SPY, QQQ, IWM (30% Barrier) | PAYH | TrueShares | High Income | 0.79% | S&P 500 Futures VT (35% Target) | PAYM | TrueShares | Defensive | 0.79% | S&P 500 Futures VT (20% Target) |

|

|

| | Risks | A balanced assessment requires understanding inherent risks: | Autocallable ETFs have a "cliff effect", meaning during severe market crashes, losses can exceed those of the underlying index. In a strong bullish market, autocallable ETFs often underperform standard long-only equity positions.

|

|

| | Ready to Plan Your Retirement? | | Knowing when to retire starts with understanding your goals. When to Retire: A Quick and Easy Planning Guide can help you define your objectives, how long you'll need your money to last and your financial needs. If you have $1 million or more, download it now. | Download Your Free Guide | | The Bottom Line | With inflation persisting above 3%, traditional fixed-income portfolios struggle to generate strong real returns. Autocallable ETFs offer a differentiated source of yield based on equity market volatility, not credit spreads or interest rate duration. | While they carry risks such as a binary "cliff" at the maturity barrier, the ETF structure makes these strategies accessible, liquid, and transparent. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|

No comments:

Post a Comment