Every ten years, we see a clear picture of an emerging sector that is obvious to outperform other sectors. For instance, we saw the telecom sector dominate the 2000s, cloud computing dominate the 2010s, and AI stocks dominate the 2020s. With many investors feeling that AI stocks are overpriced after some historic returns, they are looking for an alternative that could be undervalued. | There has been considerable excitement surrounding space exploration stocks among investors, and rightfully so, as stocks like Rocket Lab have posted returns of 200%+ in 2025. Get this right, and you're positioned for the next decade. | The space sector shares some structural similarities with AI, but operates under fundamentally different constraints. Get this right, and you're positioned for the next decade. Get it wrong, and you'll be explaining why you bought into another narrative at the top. |

|

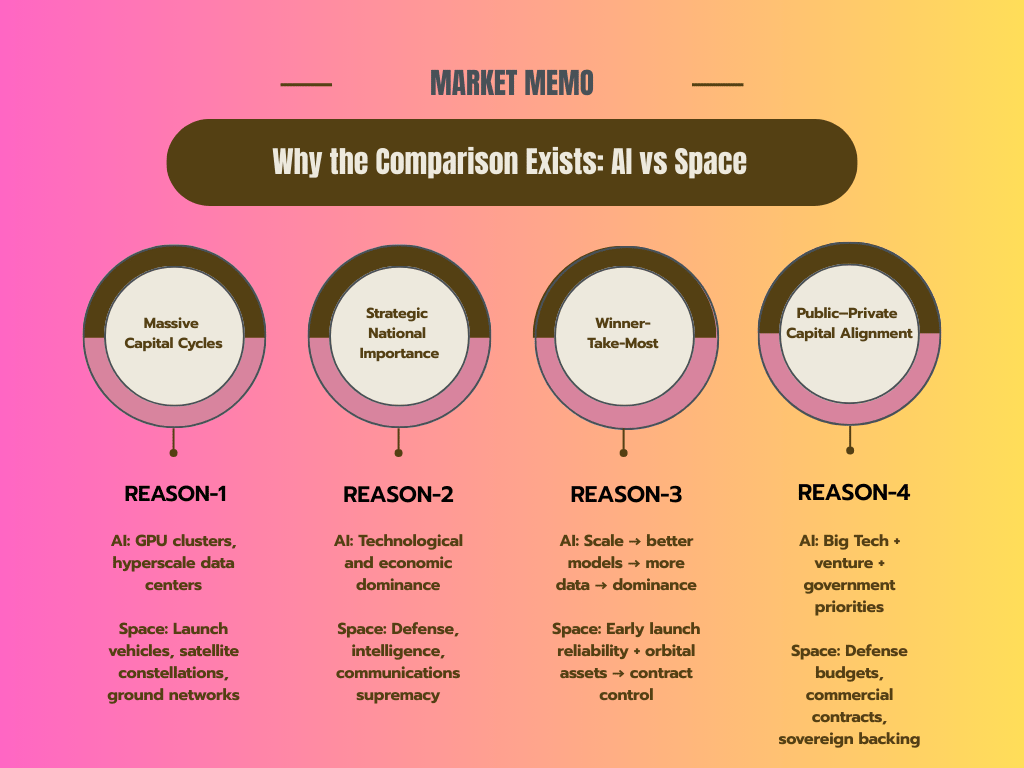

| | Why Comparison Exists Between AI And Space | AI's recent boom and the emerging space sector share multiple similarities despite the infrastructure being different, but the economic logic aligns perfectly. | |

|

| | What's Actually Driving Space | Launch costs have decreased by roughly 90% over the past decade. SpaceX's Falcon 9 changed the trajectory of the space sector when it introduced reusable rockets. The launch costs have decreased to the extent that profitability can be achieved. An explosion in low-Earth orbit satellite demand. Over the next ten years, Starlink alone plans to launch approximately 42,000 satellites. In addition to that, OneWeb, Amazon's Kuiper, and sovereign constellations from China, the EU, and other countries are also expected to undergo some major launches. Defense, surveillance, and secure communications spending. Ukraine demonstrated the tactical value of commercial satellite imagery and connectivity. Now, the U.S. is investing heavily in LEO-based communications and early warning systems. This isn't R&D anymore—it's deployment. Earth observation and data monetization. Farmers tracking crops. Insurers are monitoring storms. Logistics companies are watching ships in real-time. Industries that used to rely on guesswork are now purchasing satellite data subscriptions. That's when hardware becomes software margins. Sovereign competition. The U.S.-China dynamic around space mirrors the AI strategic competition. Both nations view space dominance as non-negotiable. That means guaranteed demand, but also fragmented markets and geopolitical constraints on who can sell to whom.

| Companies like SpaceX, Blue Origin, and Rocket Lab are building the infrastructure. NASA is the anchor customer. However, the ecosystem is still in the process of forming, and public market exposure remains fragmented and indirect. |

|

| | | | | For 22 years, each and every stock Weiss Ratings rated a "Buy" has delivered an extraordinary average return of 303% — and that includes the losers. | Our sophisticated algorithms perform millions of real-time calculations daily, analyzing over 53,000 data points per stock. | The result? Unmatched accuracy, actionable insights, and unbiased ratings — insights previously accessible only to institutional investors. | Now this eerily accurate system is flashing green on a new set of stocks… | It's identified three under-the-radar picks that could thrive in 2025 and beyond… | And we're giving away their names and ticker symbols — FOR FREE. | Click here for the names of our three top stocks to own this year (no purchase necessary). |

| |

| | |

| Here's Where The Space-AI Comparison Falls Apart | AI | Space | Fast monetization | Long monetization cycles | Software margins | Hardware + contract margins | Venture-friendly | Balance-sheet heavy | Retail narrative | Institutional + sovereign driven |

| AI had a ChatGPT moment. Overnight, everyone understood what it did and why it mattered. Revenue followed fast from OpenAI, which went from zero to billions in under three years. Space operates on a fundamentally different timeline. | AI scales infinitely once you've trained the model. Space builds rockets. One at a time. Launches satellites. One at a time. Operates ground stations. One at a time. The costs don't disappear. | Market dynamics also diverge. AI captured retail attention and venture capital enthusiasm. Space will be driven by defense appropriations, sovereign programs, and institutional telecom contracts, demand that is durable but not narratively viral. | Investors seeking rapid multiple expansion (NVIDIA-style) will be disappointed. Those comfortable with multi-year timelines and government-contract cash flows (Boeing, Lockheed Martin model) should continue evaluation. |

|

| | Who Benefits First | Let's talk about what you can actually invest in—because it's not SpaceX.\ | Start with the defense primes. Lockheed, Northrop, RTX. These entities possess the requisite security clearances, contract relationships, and balance sheet capacity for long-cycle programs. Space is quietly becoming a bigger slice of their revenue, and they're the ones landing the high-margin, multi-year government programs that actually pay on time. Satellite manufacturers are where the money gets spent. Companies producing communication satellites, Earth observation payloads, and propulsion systems receive initial capex deployment. This represents early-stage value capture but with hardware margin profiles. Launch-adjacent suppliers. Avionics, materials, ground infrastructure, and insurance providers. This layer provides diversified exposure across the ecosystem without single-provider concentration risk. Margins are stable, and demand is provider-agnostic. Space-based data and analytics. Maxar, Planet Labs, and similar entities monetize satellite-derived data for agriculture, logistics, defense, and commercial applications. This is where software-like margins emerge—but contingent on operational hardware infrastructure.

|

|

| | The Bottom Line | Space isn't going to explode as AI did in 2023. No catalytic consumer moment. No retail-driven momentum. The sector will absorb capital, contracts, and political priority incrementally while broader market attention remains on prior cycle themes. i.e., Rocket Lab's December Run. | This pattern characterizes genuine long-term infrastructure themes. They develop through sustained capex deployment, contract execution, and institutional commitment—not retail enthusiasm or narrative momentum. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|

No comments:

Post a Comment