But don’t get crazy excited yet…

Not Every Miner Wins Equally

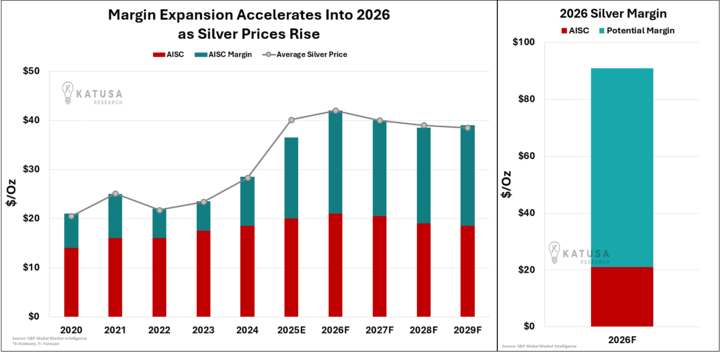

Silver stocks have been on a tear in the past year.

- The Silver Small Cap ETF ($SILJ) is up 217%. But the gap between the best and worst operators is blowing wide open.

And you have to know why you’re buying a ticker.

First Majestic for example, was losing money in 2024 with negative margins. Now they're running 45%, with production jumping over 20% and costs that dropped more than 30%. Their acquisition of Cerro Los Gatos was perfectly timed. They doubled capacity right as prices took off.

Fresnillo is projecting 52% margins, up from 26% - their costs are falling while production holds steady.

Coeur Mining expects 45%-plus after their Rochester expansion in Nevada came online.

Pan American upgraded La Colorada in Mexico and should nearly double margins to 44%.

These aren’t recommendations, but examples to show what’s happening in real-time with silver prices skyrocketing.

Then there’s Hecla, a solid operator. Their primary silver costs on a byproduct basis have risen over 20% according to S&P Global models.

In a race for pure silver leverage, they are currently lagging the aggressive margin expansion seen in peers like First Majestic.

- While the herd piles into the famous names, the real alpha is in the operators who have optimized their mines to print cash at $30 silver...

And are now absolute money fountains at $90+.

The Jurisdiction Premium

But here is where the retail crowd can get stuck, obsessing over headlines.

The "smart money" looks at the financial plumbing.

What you rarely hear discussed is the "SWAP Line" indicator.

The Federal Reserve maintains liquidity backstops with key central banks. This invisible tether keeps an economy plugged into the US financial system. It’s the difference between a volatile market and a solvent one.

.png)

No comments:

Post a Comment