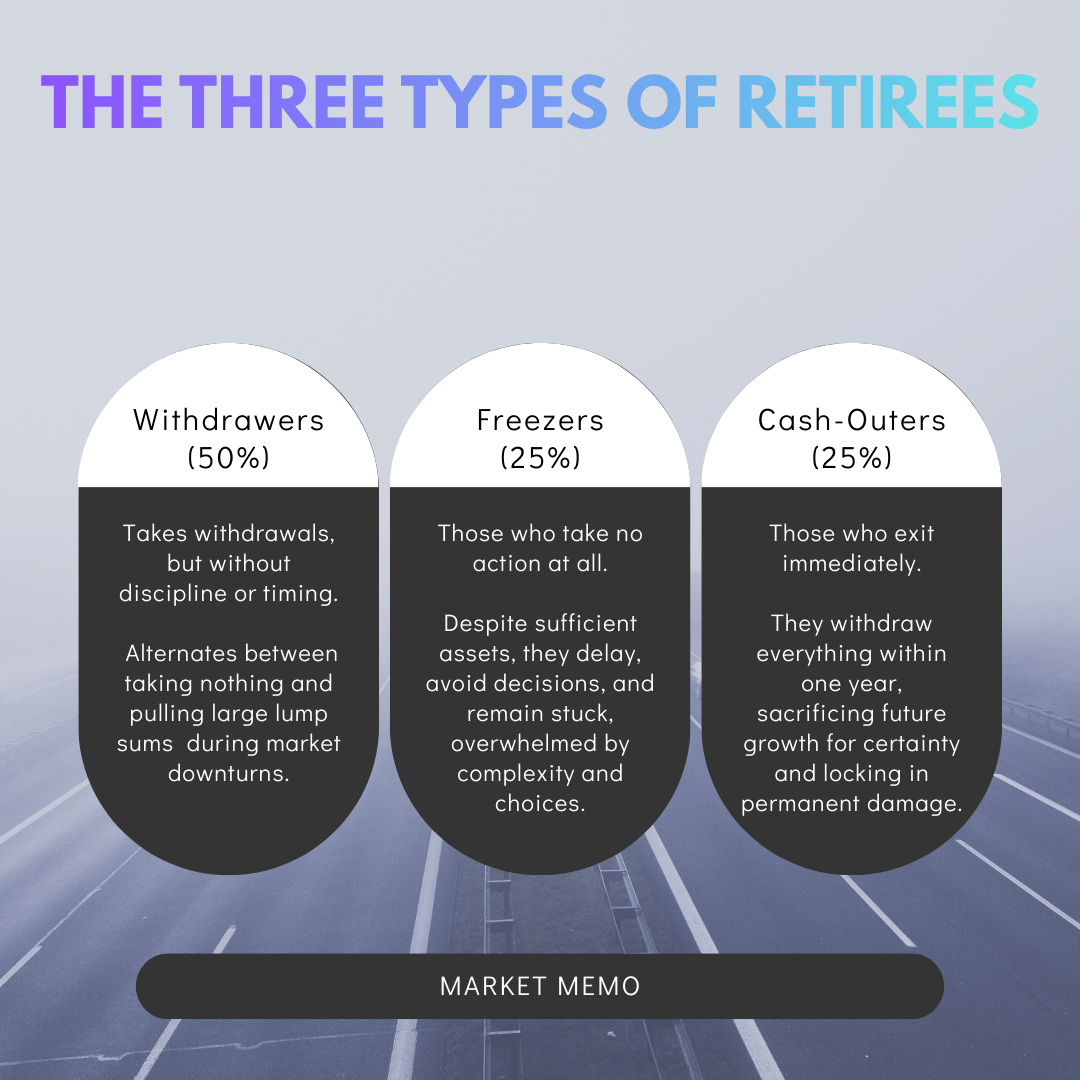

2026 is set to become the biggest year for retirements as four million Americans turn 65 in 2025. But here's the uncomfortable truth Vanguard's new research reveals: most retirees have no idea what to do with their 401(k) money once they stop working. Half take withdrawals. A quarter cash out everything immediately. And the rest? They do nothing at all, leaving hundreds of thousands sitting untouched while living paycheck-to-paycheck on Social Security. | This isn't a small problem. There's $12 trillion in defined contribution plans, covering over 100 million Americans. The accumulation phase, which involves getting the people to save money, has been largely solved through auto-enrollment and auto-escalation. The distribution phase? That's where things fall apart. |

|

| | The Three Types of Retirees | Vanguard analyzed 70,000 workers aged 60+ and found three distinct behaviors: | | Retirees in plans with flexible distribution options are 30% more likely to stay in-plan and avoid cashing out. Three years post-retirement, 75% preserve their assets. Staying in-plan provides lower fees, institutional investment options, and better withdrawal discipline. When employers make income conversion easy, retirees make better decisions. |

|

| | | | | Nvidia Chief: Where The Next AI Fortune Could Land | Nvidia's Networking Chief just revealed where he is convinced the next AI fortune could be made. | And here's the best part… You don't need to be a PhD, a Silicon Valley insider, or have millions of dollars in seed capital. | Gilad Shainer, Senior Vice President of Networking at NVIDIA, says: "A growing portion of the billions spent on AI [will land here]." | Jensen Huang, the CEO of Nvidia, agrees, calling it: "foundational to scaling AI." | Yet, these tech titans aren't talking about AI chips, chatbots, or anything like that. It's a hidden AI play few are noticing, one that's quietly becoming one of the fastest-growing cash streams in America today. | We just recorded a video on exactly where Nvidia's Networking Chief says billions could flow next… | Warning: if you're only focusing on chips and chatbot stocks, you will miss this entirely. | P.S. Nvidia just announced it will spend $500 billion over the next. | 4 years… But a massive chunk of that cash is headed somewhere surprising. | It's not AI chips, chatbots, or anything similar. Yet Nvidia's own Networking Chief says fortunes could be made here. Click here to watch the full story now. |

| |

| | |

| The Generational Divide | Gen Z (47% on track): Best-positioned despite student loans and credit cards consuming 25% of their median income. Auto-enrollment and escalation features are working. Millennials (42% on track): Carry twice the non-housing debt boomers had at their age, yet stronger plan design compensates. Time is their advantage. Baby Boomers (40% on track): The top 30% are fine. Everyone else faces a median annual shortfall of $9,000—nearly a quarter of their expenses.

|

|

| | The Income Problem | Lower-income Americans face a brutal reality: even with Social Security replacing most income, fewer than one in six earning $22,000 or less annually are on track for retirement. Why? Their spending in retirement won't be much lower than pre-retirement spending. There's no fat to trim. | This creates a bifurcated system where wealthy retirees manage multiple accounts and optimize tax strategies, while low-income retirees struggle to maintain basic living standards despite doing "everything right" by saving what little they can. |

|

| | 6 High-Impact Retirement Actions | | The Access Gap | If all workers had defined contribution plan access, 6 in 10 Americans would be retirement-ready. Currently, only 4 in 10 are. That 20-point gap represents millions facing insecurity due to employer plan availability, not personal failings. Policy matters more than individual behavior modifications. |

|

| | The Bottom Line | The retirement system in America is simultaneously getting better and remaining deeply flawed. Younger generations benefit from smarter plan design and behavioral nudges. But the distribution phase, where accumulated wealth becomes spendable income, remains a black box for most retirees. | The encouraging news is that even small changes produce meaningful results. Working two more years, staying in-plan rather than cashing out, and maintaining consistent (rather than erratic) withdrawals can transform retirement outcomes. | The sobering reality: most Americans are winging it. With 4+ million people retiring annually and $12 trillion at stake, the industry needs systematic solutions for the decumulation phase that match the sophistication we've achieved in accumulation. | For individuals approaching retirement: the math isn't as complicated as the industry makes it seem. Stay in your employer's plan if it offers good withdrawal options. Take steady, modest distributions rather than lumpy withdrawals. Work a bit longer if possible. And for the love of compound interest, don't cash out your entire 401(k) the day you retire. | Your 65-year-old self will thank you. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|

No comments:

Post a Comment