Dear Reader,

Can you still profit from the current stock market?

According to Weiss Ratings, the answer is yes …

IF you invest in the right stocks.

Keep in mind, Weiss Ratings was ranked #1 by both the SEC — the authority that regulates the stock market — and the Wall Street Journal, the world's foremost stock market publication …

And for good reason …

Because when it comes to profits for investors, nobody can beat the Weiss Ratings track record:

|

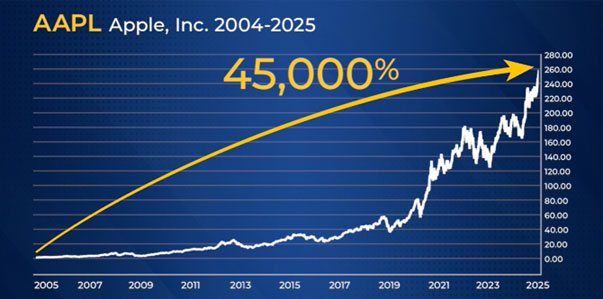

It identified Apple at 50 cents — it's up over 45,000% since …

|

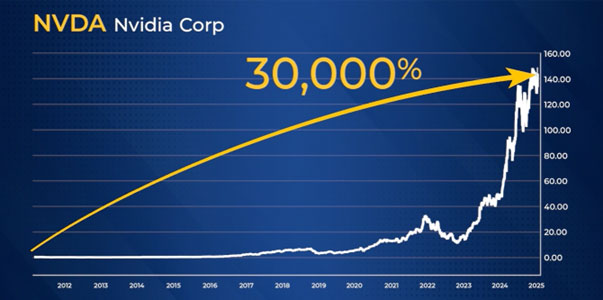

Nvidia at 40 cents — up 30,000% today …

|

And Netflix at $3.70 — now up more than 27,000% …

But this is just a small sample …

For over 20 years, Weiss Ratings' picks have made an average gain of 303% — including the losers.

And now, this eerily accurate system is flashing green on a new set of stocks …

Specifically, it identified three under-the-radar picks that could thrive in 2025 and beyond …

And we're giving away their names and ticker symbols — FOR FREE.

That's right, if you missed out on the 3x … 5x … or even 10x gains of the past years …

This could be your best chance to make it right.

Make sure you don't miss it.

Sincerely,

Eliza Lasky

Weiss Advocate

PS:

Every time Weiss Ratings flashed green like this, the average gain on each and every stock has been 303% (including the losers!).

Click here for the names of our three top stocks to own this year (no purchase necessary).

Oracle Has Spoken: AI Changes Everything

Written by Thomas Hughes. Published 9/10/2025.

Key Points

- Oracle's Q1 results and guidance update affirm a ballooning outlook for AI and hyperscale demand.

- Analysts are lifting their targets and forecast a move above $400.

- The guidance is mostly booked; investors should expect it to continue growing.

Anyone surprised by Oracle's (NYSE: ORCL) Q1 guidance update hasn't been paying attention to the steady stream of news. Oracle's forward-looking metrics have accelerated for over a year as it expands AI-enabled services for developers and enterprise applications.

The critical takeaway is that Oracle is no longer a niche database provider among many options. It has become a vital link in AI infrastructure globally and now stands as a hyperscaler to be contended with.

2013 Bitcoin miner reveals his trading system (free) (Ad)

While everyone else is gambling on meme coins or chasing the next "100x moonshot," our members are systematically extracting profits from the $4 billion that changes hands in crypto every single day.

Claim Your Free Trade Alert →The Q1 release highlighted strong demand from existing hyperscalers—Amazon, Google and Microsoft—and the robust growth they bring. Oracle chairman and CTO Larry Ellison reported that revenue from these three grew by more than 1,500% in Q1 and is expected to remain strong over the next few years.

He forecasts Oracle's datacenter footprint will more than double, driving substantial growth each quarter for years to come.

Oracle's Miss Overshadowed by Strong Guidance, Accelerating RPO

Oracle's Q1 results fell short of analysts' forecasts, but two factors more than offset the miss. First, total revenue rose 12.3% year over year to nearly $15 billion, accelerating sequential growth as demand for cloud infrastructure surged.

Second, the outlook was jaw-dropping, with guidance implying a 359% increase in remaining performance obligation (RPO).

CEO Safra Catz noted that most of this guidance is based on signed contracts, with more multi-billion-dollar hyperscale deals in the pipeline. In this context, management's outlook may even prove conservative, and growth could exceed these robust projections.

Segmentally, Oracle's cloud business was the standout. Q1 cloud revenue rose 28%, driven by a 55% jump in infrastructure-as-a-service (IaaS) and an 11% increase in software-as-a-service (SaaS). Within SaaS, Fusion ERP grew 17% and NetSuite 16%.

Margin news was mixed, but guidance offsets the concerns. Adjusted EPS climbed 6% to $1.47—just a cent below MarketBeat's consensus—despite top-line softness.

Looking ahead, profits are poised to improve significantly, with strong revenue leverage likely to boost earnings in upcoming quarters.

As of early September, analysts forecast Oracle's annual growth to accelerate to about 35% by 2028—a number we believe is conservative. Oracle expects its cloud business to deliver triple-digit growth for at least two years, then sustain a robust pace for the following three years.

With the cloud segment already accounting for roughly half of net revenue, sustaining triple-digit growth translates to about 50% growth relative to the Q1 baseline.

Oracle's Bullish Analyst Sentiment Expected to Strengthen in Q3 and Q4

Analysts' initial reaction to Oracle's guidance was stunned silence, followed by a wave of price-target hikes. Many lifted their targets by 20% to 30%, establishing a new high-end range that implies roughly a 70% gain from pre-release levels.

While the stock's 30% advance post-release has captured some upside, significant potential remains for investors. Analysts are likely to raise their targets further as Q3 and Q4 unfold, potentially boosting both the high-end and consensus estimates.

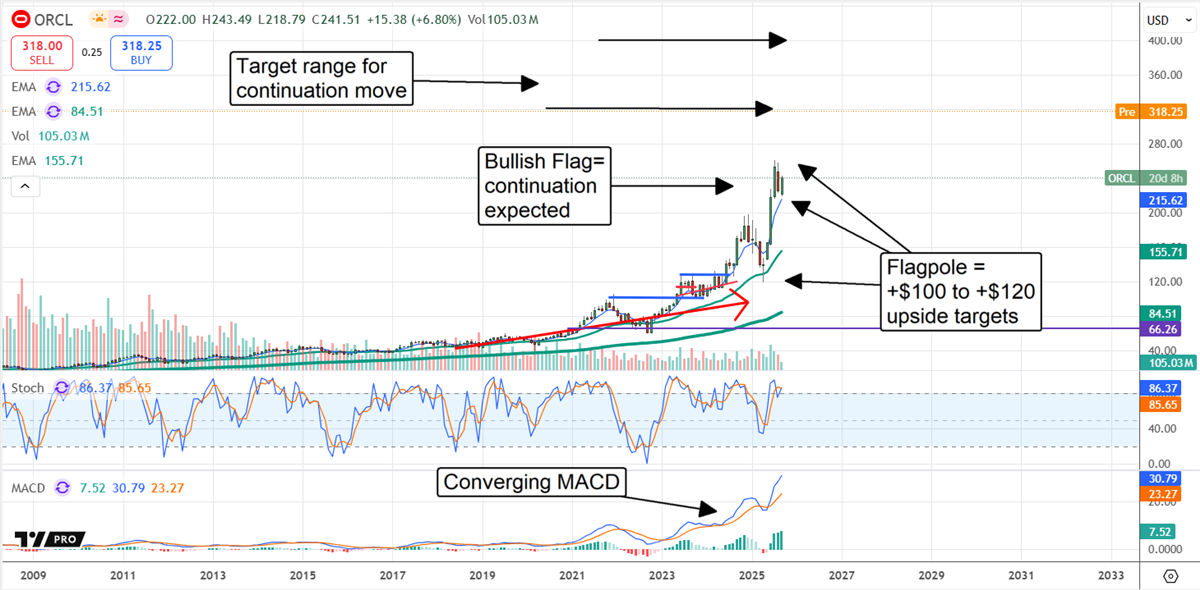

The stock's technical setup was bullish heading into the release, with the market in rally mode and MACD converging across multiple time frames. For more details, see our analysis of Oracle's 2025 rally.

The $75 (30%) gain represents about 75% of the indicated potential, suggesting Oracle could reach the $340 region before encountering its first major resistance level.

to bring you the latest market-moving news.

This email is a paid advertisement sent on behalf of Weiss Ratings, a third-party advertiser of TickerReport and MarketBeat.

11780 US Highway 1,

Palm Beach Gardens, FL 33408-3080

Would you like to edit your e-mail notification preferences or unsubscribe from our mailing list?

Contact Us | Unsubscribe

Copyright 2006-2025 MarketBeat Media, LLC dba TickerReport. All rights reserved.

345 North Reid Place, Suite 620, Sioux Falls, South Dakota 57103. United States..

No comments:

Post a Comment