We have discussed two important bottlenecks before, but the biggest bottleneck in the AI supply chain right now is not wafer fabs or chip design but advanced packaging. It is the answer to why the markets' trillion-dollar ambitions are waiting 18 months for a free slot. The single process that is quietly beginning to decide the winners of the AI race. |

|

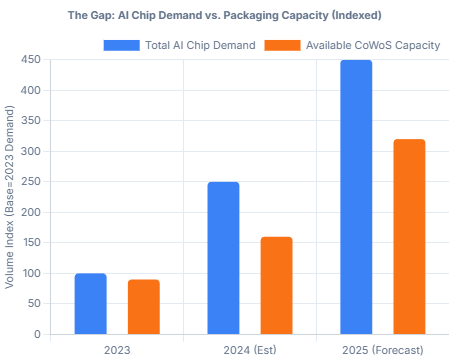

| | The Irony That's Costing Billions | The world is sitting on a massive output. All the semiconductor companies are working overtime to make the most of it. Fabs and chips are ready too. But the flow has hit a huge bump – packaging. |  | AI chip demand and packaging capacity |

| Packaging queues stretch 12-18 months deep. Billions of dollars' worth of inventory are in their work-in-progress stage, which is just not progressing quickly. Because Hyperscalers make bookings a year ahead. And what's more? The utilization never goes below 95%. | Imagine you have ordered a perfect meal from a Michelin-star chef. It's cooked and ready to be served. But the person who can serve it to you says he is booked through next summer. |

|

| | | | | The only stock picking system in America that we know of has been ranked #1 for profit track record by both — the Wall Street Journal and the SEC. | And while some of the current AI top dogs are getting crushed.This eerily accurate system is flashing green on a new set of stocks. All of which could become the biggest winners of 2025 and beyond. | Specifically, Weiss Ratings identified three under-the-radar picks that could thrive in the next stage of the AI boom. | And we're giving away their names and ticker symbols for FREE. | If you missed out on the recent windfall … |

| |

| | |

| The Silicon Puzzle That Changed Everything | Modern AI processors are chiplet clusters that require precision assembly. | One AI GPU contains: | 1 logic die on a bleeding-edge node. 6-8 HBM stacks with each containing 8-16 DRAM dies. Thousands of microbumps and TSVs connecting everything. A silicon interposer up to 2,500 mm² in size.

| Screw up the contents in the assembly, and your AI accelerator becomes a very expensive paperweight. But here's where the economics is thrown at: each GPU consumes the packaging capacity that used to serve hundreds of consumer chips. |

|

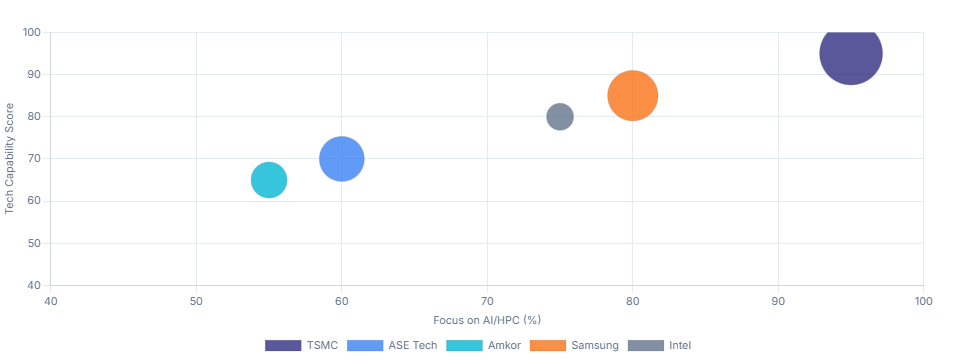

| | The Numbers That Should Terrify Your Portfolio | The advanced packaging market is valued at close to $40 billion in 2025 and heads toward $80 billion by 2034. That's 7.5-8.5% annual growth. | But there is another version to story. One that involves the AI packaging segment exploding at 26% CAGR through 2033 – three times faster than the overall semiconductor industry. |  | Competitive landscape positioning |

| Before leaning into any story, let's check the capacity math: | TSMC's CoWoS output today: 75,000-80,000 wafers/month. Target by late 2026: 120,000-130,000 wafers/month. Already locked by top customers: 85%+. Some hyperscalers alone are consuming: 60%+ of premium capacity.

| And this clearly states the brutal reality – AI demand rises 50% year-over-year. Packaging capacity grows in single digits. |

|

| | The $1,300 Problem | Packaging costs for high-end AI chips are anticipated to hit $1,300 per unit. Make an error, and that $1,300 goes to waste. Interposer and substrate pricing have gone up between 30% to 40% since 2023. HBM now represents nearly 40% of the total bill-of-materials for some accelerators. | Alongside the costs, the delivery time stretches, but expands the margin for the gatekeepers. TSMC, Samsung, and the OSATs do not complain. But everyone else has a different story. |

|

| | Three Reasons This Gets Worse Before It Gets Better | 1. HBM Supply Is Redlining | SK Hynix, Samsung, and Micron are the only three companies supplying every HBM stack on Earth. What does this mean? A 200%+ rise in demand from 2023 to 2025. The suppliers could not yet meet the demand. With a supply deficiency, perfect wafers are sitting untouched. | 2. Substrates Are the New Unobtainium | ABF substrate capacity reaches $15.8 billion in 2024. The market anticipates a growth of $31.1 billion by 2033. It's still not enough, because materials themselves remain scarce. GPU shipments are delayed by a whole financial quarter owing to interposer shortages. With control shipments, companies like Ibiden, Shinko, Unimicron, and Nanya PCB become the new kingmakers. | 3. New Capacity Takes Forever | Building a new packaging capacity is a great idea. But with the equipment delivery taking 12 to 18 months and qualification adding another 6 to 12 months, it will take over 2 years before you can ship real products. Suppliers' optimistic view shows a crunch till 2027. |

|

| | The New Power Hierarchy | TSMC: The Center of Gravity | TSMC's CoWoS is at the heart of AI production, witha single generation of NVIDIA and AMD GPUs consuming huge capacity: | NVIDIA Blackwell: 1 logic tile + 6 HBM stacks per GPU. CoWoS demand growing 30%+ annually. Entire GPU supply dependent on CoWoS access.

| Yet, TSMC's massive expansion plans are insufficient in matching AI adoption. | Samsung: The Vertical Fortress | Under one roof, Samsung controls logic, HBM, and packaging. Its I-Cube and X-Cube platforms offer escape routes for customers seeking alternatives to TSMC. | Suddenly, vertical integration becomes a genius strategy. | ASE, Amkor, JCET: The OSAT Revolution | These outsourced assembly houses are developing into high-power players: | ASE's CoWoS-equivalent capacity targeting 20,000-25,000 wafers/month. Amkor's advanced packaging share could double by 2033. OSATs are now essential for anyone squeezed out of TSMC's queue.

| Whether they wanted to or not, they are being pulled into the center of AI infrastructure strategy. |

|

| | The New Market Reality: Haves vs. Have-Nots | The Winners | The Losers |

|---|

Firms holding scarce packaging slots – shipping products while competitors wait. | Small/mid-tier chip designers – unable to secure slots at any price. | Substrate suppliers (Ibiden, Shinko) – gaining unmatched pricing power. | AI startups – slipping 6–12 months behind schedule, burning runway. | Packaging equipment makers – orders up more than 20% in 2024. | Hyperscalers without pre-booked deals – waiting quarters for delivery. | Memory suppliers controlling HBM – SK Hynix laughing all the way to the bank. | Companies with idle wafers – burning capital in WIP limbo. |

| Their margins rise with scarcity, which isn't temporary. Now that there is a thicker line between companies with packaging access and those that lacks them, the success of your portfolio will be based on which side you're on. |

|

| | The Bottom Line | Wafer fabs continue to be a limiter. However, the pace of AI advancement, including GPU shipments, data center expansion, and model rollouts, gives power to packaging throughput. | AI companies want scalable compute. And it is packaging that decides the final count and the shipping date, strongly influencing even the revenue. Ultimately, it decides which companies surge and which stall. | So, a diverse portfolio that considers the limited powerhouses in the packaging sector might be a worthy shot at market gain. |

|

| | | | | Important disclosures: This newsletter is provided for informational purposes only and does not constitute investment advice. All investments involve risk, including possible loss of principal. Please consult with your financial advisor before making investment decisions. |

| |

| | |

|

|