Why the Latest Inflation Numbers Look Hideous – And May Get Worse…VIEW IN BROWSER In the 1970s, gas lines became a symbol of inflation Americans could see with their own eyes. We are not back in that world. But investors are getting a reminder of how fast energy prices can rise when geopolitics turn ugly. According to AAA, the national average for regular gas has climbed from $2.98 a gallon on February 26 to about $4.16 now. And while markets initially cheered news of a two-week ceasefire with Iran, that ceasefire already looks like it is hanging by a thread as oil prices swing around every new headline. That matters because higher energy costs rarely stay at the pump. They tend to spread through shipping, travel, food and a long list of everyday expenses. Which is why this week’s inflation data is so important. Investors are looking at the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index for clues about where inflation stands now. But I should mention that this data looks backward. It tells us where inflation was, not necessarily where it is headed if energy costs keep pushing higher. And I’ll be honest with you – the numbers are hideous, as I suspected they would be. So in today’s Market 360, I want to walk you through what the CPI and PCE reports are really telling us, what they may be missing and what the implications could be for the Federal Reserve, key interest rates and your portfolio.

Recommended Link |

|

The AI boom has been stalled for months. But according to legendary tech investor Louis Navellier, that’s about to change. How? A $100 trillion breakthrough is about to reset the AI markets in 2026… potentially sending some AI stocks to zero, and one off-the-radar stock soaring. Click here for details and Louis’ top pick — free. |

|

|

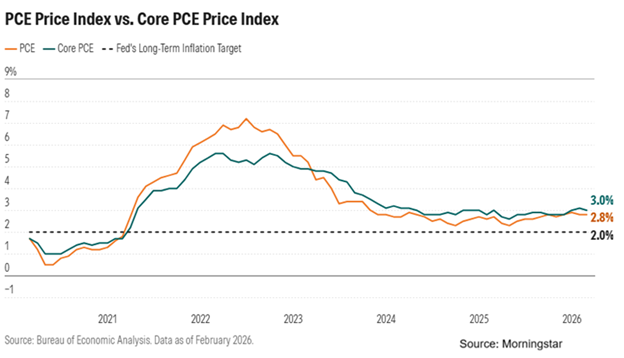

What the Data Is Telling Us – and What It Isn’t…Let’s start with the PCE, the Fed’s favorite inflation indicator. Now, this delayed report showed that headline PCE rose 0.4% in February and is now up 2.8% year-over-year – right in line with expectations. Core PCE, which strips out food and energy, came in at 3.0% year-over-year, also rising 0.4% for the month. That’s still well above the Fed’s 2% target.

So, this shows that inflation was already stubborn before energy prices began moving higher. The conflict with Iran escalated late in February, so much of the recent jump in energy costs hasn’t yet shown up here. Then came CPI – and it showed energy is starting to bite. Headline CPI rose 0.9% in March, the biggest monthly increase since 2022, while energy prices soared 10.9%. Gasoline prices jumped 18.9% and fuel oil prices surged 44.2%. Core CPI, which excludes food and energy, increased 0.2% last month and was up 2.6% in the past 12 months.

Interestingly, the headline CPI was in line with economists’ expectations, and the core CPI was better than expected, rising 0.3%. Overall, higher energy costs are clearly starting to show up. So, here is the key point: These reports show inflation was already stubborn, and they also show higher energy costs are starting to work their way into the economy. But that may not be the full story, either. Much of the recent surge in oil and gas prices happened late in the month and into April, so the full impact may still be ahead. Which means inflation could remain more stubborn than investors expect. What This Means for the Fed and InvestorsWhat needs to happen now is for traffic in the Strait of Hormuz to return to pre-conflict levels and for the U.S.-Iran negotiations to be fruitful. When that happens, uncertainty will diminish further, inflation will moderate and things can get back to normal. Until that happens, the inflation numbers are likely to be hideous. So, what does this mean for the Fed and for investors? It means the Federal Reserve may not have much room to cut rates anytime soon. Inflation is still above target. And if higher energy costs keep working their way through the economy, that could make it even harder for the Fed to ease policy in the months ahead. In other words, interest rates could stay higher for longer than many investors expect. And that matters because markets can handle high rates for a while. But when investors start to realize rates may stay elevated longer than expected, leadership often begins to shift. We saw that in the early 2000s, when the biggest tech winners stopped leading. Other parts of the market still moved higher. But many investors who were heavily concentrated in those former leaders went through years of flat returns. That is the real risk here. It is not just that inflation stays stubborn. It is that stubborn inflation can keep pressure on rates – and higher-for-longer rates can expose risks that were easy to ignore when money was cheap. That’s when concentration starts to matter a lot more. And right now, I believe many investors are far more concentrated in Big Tech than they realize. That creates the potential for what I call a “Hidden Crash.” It’s not a big drop you see on the news. But it can lead to years of flat or disappointing returns for investors who think they’re diversified but really aren’t. And if you’re invested in yesterday’s tech winners right now, it’s something you may need to think about. That’s why I put together a full breakdown of what I’m seeing – including why I believe money is starting to move out of Big Tech and into a group of what I call “edge innovators” – companies that stand the most to benefit from this shift. You can go here to learn more about them now. Sincerely, |

.png)

.png)

Tiada ulasan:

Catat Ulasan